Contents

- Singapore’s Mandatory ESG Reporting Requirements: Key Components

- What is the Enterprise Singapore and EDB Sustainability Reporting Grant (SRG)?

- Sustainability Reporting Grant Application Process: Step-by-Step Guide

- Eligibility and Application Checklist

- How will the funds be released?

- What are common pitfalls to avoid when applying?

- The SRG vs. Other ESG Grants for SMEs in Singapore

- How can the SRG help with ISSB-aligned ESG reporting?

- How Presgo Can Support SRG-Aligned Sustainability Reporting

Singapore’s ESG reporting landscape is shifting from a ‘comply-or-explain’ approach to mandatory, global-ready climate-related disclosures. Compliance with the ISSB is now critical, as it underpins regulatory filings, investor expectations, and access to support like the Sustainability Reporting Grant.

The grant helps Singaporean companies build their first ISSB reports and prepare against future regulatory shifts, forming foundations for strong sustainability reporting. Below is a guide to the Sustainability Reporting Grant and how it can support ISSB-aligned ESG reporting.

Singapore’s Mandatory ESG Reporting Requirements: Key Components

Singapore still focuses its mandatory ESG reporting on climate-related disclosures. The core requirements sit under the Singapore ISSB-based climate reporting roadmap, which is being phased in from FY2025 onwards and applies mainly to listed companies and, later, large non-listed companies.

For listed companies, the mandatory climate-related disclosures are broadly aligned with ISSB’s IFRS S2 Climate-Related Disclosures and cover:

- Scopes 1 and 2 greenhouse gas (GHG) emissions

- Mandatory for all SGX-listed firms from FY2025

- Climate-related risks and opportunities

- Governance, strategy, and risk management processes for climate-related issues must be disclosed.

- Scope 3 emissions

What is the Enterprise Singapore and EDB Sustainability Reporting Grant (SRG)?

The Enterprise Singapore and the Economic Development Board (EDB)’s Sustainability Reporting Grant (SRG) is a co-funded programme designed to help Singapore-incorporated companies prepare and publish their first ISSB-aligned sustainability report, especially as they gear up for Singapore’s mandatory climate-related disclosure rules.

The SRG:

- Provides up to 30% of co-funding of qualifying costs, capped at S$150,000 per company, whichever is lower.

- Covers expenses such as consultancy services, manpower training, software and tools, and external assurance for scopes 1 and 2 emissions to support the production of an ISSB-aligned sustainability report.

Qualifying costs of the SRG

The SRG is designed to cover expenses directly tied to producing and verifying the first ISSB-aligned sustainability or climate report. Typical qualifying cost categories include:

- Consultancy services

- Fees paid to external consultants or advisors for materiality assessment and disclosure scoping, data-gathering and mapping for ISSB disclosures, and drafting and structuring the sustainability report.

- Manpower training

- Training for internal staff on ISSB standards and ESG reporting frameworks, data collection, GHG accounting, climate risk assessment, and reporting tool usage.

- Software and tools

- Licenses or subscriptions for ESG reporting platforms, carbon accounting software, or data management tools specifically used for the first ISSB-aligned report.

- External assurance

- Assurance fees for scopes 1 and 2 emissions performed by a qualified third-party assurance provider, where the assurance is part of the first-time ISSB-aligned reporting effort.

Who can apply for the SRG?

The core eligibility criteria for organisations that can apply for the SRG include:

- Singapore-incorporated companies only. This includes all SGX-listed companies regardless of revenue size, not just large blue-chips. Foreign-registered entities or mere branches are not eligible on their own.

- Non-listed Singapore-incorporated companies with annual revenue of at least S$100 million.

The SRG is aimed at large local firms and listed companies that are either already in scope or will soon be for Singapore’s ISSB-based climate-related disclosure rules.

The grant is not limited by industry or sector. It is open to any qualifying Singapore-incorporated company, such as industrial, real estate, or financial services, as long as they meet the listing or revenue thresholds.

On the other hand, SMEs with revenue below S$100 million do not qualify for the SRG. Instead, these companies can access a separate SME Sustainability Reporting Programme. Companies that have already published a comprehensive sustainability report may also not qualify, since the SRG specifically targets first-time, ISSB-aligned reporting projects.

When can companies apply for the grant?

Companies can apply for the SRG on an ongoing, open-window basis, rather than a fixed period. The SRG was launched in November 2024 and remains open for eligible applicants as they progress toward their first ISSB-aligned sustainability report.

Eligible companies with at least 30% local shareholding apply via Enterprise Singapore’s Business Grants Portal, under the SRG listing. Other eligible companies, such as more foreign-controlled entities, can apply through EDB’s grant/incentives channels, using the same eligibility criteria and funding cap.

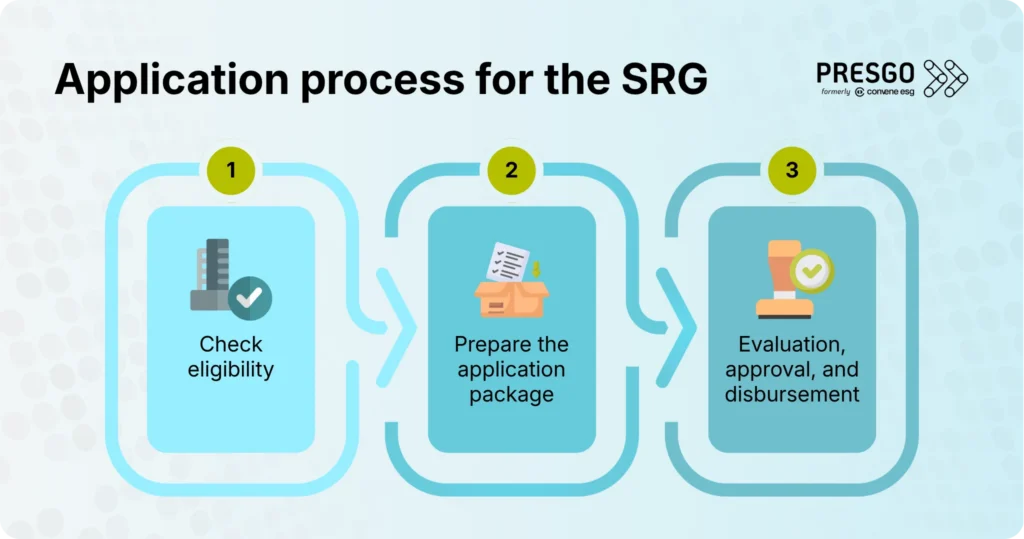

Sustainability Reporting Grant Application Process: Step-by-Step Guide

The application process for the Enterprise Singapore-EDB Sustainability Reporting Grant follows a standard government-grant workflow but is split depending on the company’s shareholding structure. Singapore-incorporated companies with at least 30% local equity apply via Enterprise Singapore’s Business Grants Portal, while companies with less than 30% local equity can contact the Economic Development Board directly to submit a formal application for the grant.

The typical application process goes as follows:

- Check eligibility

Before applying, organisations should confirm that they are Singapore-incorporated and either SGX-listed or a non-listed company with an annual revenue of S$100 million or higher. Likewise, the company should be preparing for its first ISSB-aligned sustainability or climate-related report instead of an already aligned report.

Key conditions that would make a company ineligible for SRG include:

- The company is not Singapore-incorporated.

- The company is neither SGX-listed nor has an annual revenue of S$100 million or higher.

- The company has already published a comprehensive, ISSB-aligned sustainability report.

- The planned report is not aligned with ISSB standards.

- The project is outside Singapore’s supportable climate-disclosure timeline.

- Prepare the application package

Typical requirements include company details, a project plan describing the scope of the first ISSB-aligned sustainability report, and cost estimates for qualifying expenses with a clear breakdown of how much will be claimed under the 30%-up-to-S$150,000 cap. Documents typically required for the SRG application are as follows:

- UEN and ACRA business profile or certificate of incorporation

- The latest audited financial statements to confirm revenue

- SGX listing confirmation or listing number

- Shareholding register or ACRA extract showing local vs foreign ownership

- Project plan outlining objectives, scope, timeline, and key milestones

- Detailed budget for qualifying costs

- Consultancy fees

- Software/tools costs

- Training costs

- External assurance fees

- Quotations or engagement letters from consultants, assurance providers, and software vendors

- Completed EnterpriseSG/EDB application forms

- Declaration that the project is for the first ISSB-aligned sustainability report and aligns with Singapore’s climate-disclosure timeline

- Evaluation, approval, and disbursement

EnterpriseSG and EDB will review the application, typically within a few weeks, for eligibility, project feasibility, and alignment with ISSB standards. If approved, the company proceeds with the project.

After incurring qualifying costs, the organisation can submit claims to receive the 30% co-funding, up to S$150,000. Before disbursing the grant, EnterpriseSG conducts an audit and verification of the claim to confirm that the costs are eligible and qualifying under SRG; are accurate and supported by valid invoices and proof of payment; that the project was executed within the approved scope and timeline; and that the company has complied with all grant terms and conditions, including any required final reports or declarations.

Eligibility and Application Checklist

Use the checklist below to confirm your company’s eligibility and help prepare key documents and details needed to apply for the SRG:

How will the funds be released?

The SRG funds are released on a reimbursement basis after costs are incurred and proper documentation is submitted, not as an upfront lump sum.

Funds are typically released following this process:

- The company gets approval for the SRG application and then proceeds to spend on qualifying activities.

- After incurring the costs, the company submits claims with supporting documents such as invoices, proof of payment, and a brief expenditure or progress report via the EnterpriseSG Business Grants Portal or EDB’s grant channels.

- EnterpriseSG or EDB then reimburses up to 30% of qualifying costs, capped at S$150,000, in one or more instalments depending on the project timeline and total eligible spend.

What are common pitfalls to avoid when applying?

For companies using and applying for the SRG, common pitfalls typically involve the grant process discipline and ESG reporting practice. Below are the most common ones to avoid:

Treating SRG like a “blank cheque”

Only clearly defined qualifying costs are funded. Internal salaries, branding, or generic overheads are not included. Organisations should align the project scope tightly with SRG definitions and document each cost as “reporting specific” from day one.

Starting the grant and project too late

SRG is reimbursement-based and tied to work within Singapore’s climate-disclosure timelines. Delaying the process may raise the risk of missing the window for support. It’s recommended that organisations apply and secure approval 6-12 months before the target reporting data to accommodate data gathering, consultant work, and assurance.

Inadequate documentation and record-keeping

Grant authorities need to trace each cost back to the first ISSB-aligned report. To avoid this, organisations should maintain a simple tracker that records the type of cost, vendor, invoice, and purpose linked to SRG deliverables. A concise narrative showing how expenses support the report is also crucial.

Over-promising and under-scoping

Grant reviewers may reject applications that look like general strategy or digital transformation initiatives rather than a defined, time-bound reporting project. Organisations should scope the project narrowly around materiality, baseline data, draft report, and limited assurance, along with clear milestones and deliverables.

Misaligning with ISSB or local requirements

SRG is for the first ISSB-aligned report. As such, a report that isn’t aligned with S1/S2 will not meet the core intent and may not pass audit or be claim-eligible. Organisations are advised to use ISSB templates and guidance early and get a quick alignment check from a consultant familiar with Singapore’s ESG landscape when possible.

The SRG vs. Other ESG Grants for SMEs in Singapore

The SRG sits alongside other ESG-related grants for SMEs in Singapore, such as EnterpriseSG’s SME Sustainability Reporting Programme. These grants generally target smaller companies or different aspects of sustainability, such as energy, tech, or transformation. However, there are still distinct differences between SRG and other ESG grants in the country.

| Feature | SRG (Large companies/listed) | SME Sustainability Reporting Programme | Other ESG- or green-tech grants (SMEs & mid-caps) |

| Target companies | SGX-listed firms and non-listed Singapore-incorporated companies with S$100M revenue or higher | SMEs below S$100M in revenue preparing their first sustainability report | SMEs and mid-caps investing in energy efficiency, green tech, or decarbonisation projects |

| Primary focus | First ISSB-aligned sustainability or climate-related report in anticipation of Singapore’s mandatory ESG-climate rules | Helping SMEs prepare their first sustainability report using frameworks such as GRI or TCFD, with pre-screened advisors | Operational improvements, such as solar, energy-efficient equipment, EV-charging, or low-carbon transport |

| Type of support | 30% co-funding of qualifying costs, capped at S$150,000 per company | Fee-subsidy model: EnterpriseSG defrays 70% of eligible advisory costs, then 50% up to October 2027 | Usually reimbursement or post-project payout after qualifying equipment or work is installed and verified |

| Typical use case | Large or listed companies preparing their first ISSB-aligned sustainability or climate report | SMEs taking their first step toward formal ESG reporting, with subsidised advisory | SMEs upgrading facilities, fleets, or processes to reduce environmental impact and operating costs |

How can the SRG help with ISSB-aligned ESG reporting?

The SRG is specifically designed to help Singapore companies build capability and capacity for ISSB-aligned ESG reporting. Below are some of the ways it helps in practice:

Covers the upfront cost of ISSB-aligned reporting

SRG’s 30% reimbursement of qualifying costs helps make the first-time transition to ISSB financially feasible, especially for large but non-listed companies that do not yet have mature ESG teams.

Builds internal ESG reporting capabilities

SRG covers manpower training for staff on ISSB principles and other ESG disclosure requirements. By investing in training and external advisors, companies can internalise ESG reporting rather than rely entirely on consultants every year.

Supports assurance-ready climate disclosures

SRG supports external assurance of scopes 1 and 2 emissions, which is a core part of ISSB-aligned climate-related reporting. Working with an assurance provider under the SRG helps improve data quality, identify gaps in monitoring and controls, and strengthen credibility with investors and regulators in Singapore.

Aligns with Singapore’s regulatory roadmap

SRG is timed to help companies align with Singapore’s ISSB-based climate-reporting roadmap, including scopes 1 and 2 for all listed firms from FY2025, and the addition of scope 3 for STI constituents from FY2026. SRG can help test materiality assessments, data flows, and narratives under ISSB.

Encourages structured ESG governance

The SRG pushes management to formalise ESG governance by defining the report’s scope, data sources, and responsibilities, and other project milestones and deliverables. This can be essential for any serious ISSB-based ESG reporting framework.

How Presgo Can Support SRG-Aligned Sustainability Reporting

Aligning with the Sustainability Reporting Grant helps qualified companies future-proof against Singapore’s mandatory ISSB-based climate-related disclosures while substantially defraying the upfront cost of their first aligned sustainability report. It also builds internal ESG reporting capability and strengthens credibility with investors and regulators through structured, assurance-ready ESG disclosures.

Presgo is an AI-first ESG reporting software that simplifies SRG-aligned reporting by turning the grant-funded “first ISSB-aligned report” into a repeatable and scalable process rather than a one-off exercise.

Taking advantage of features such as pre-built templates, emission calculations, and data centralisation allows eligible companies to use SRG more efficiently, generating ISSB-aligned reports faster and embedding them into business operations and strategy.

Request a demo today to maximise the benefits of SRG with Presgo!