Contents

- Why is Singapore adopting the ISSB Standards in sustainability reports?

- But, are Singapore companies ready for ISSB-aligned climate disclosure?

- How to Prepare for Singapore Sustainability Reporting: 10 Steps for ISSB Compliance

- 1. Understand the Singapore reporting obligations and your reporting gaps

- 2. Identify gaps and choose the right tools

- 3. Identify material issues and create a materiality matrix

- 4. Get leadership buy-in

- 5. Run climate scenario analysis

- 6. Build the emissions inventory and sustainability metrics

- 7. Set ESG targets and policies

- 8. Structure the report around the four ISSB pillars

- 9. Prepare for assurance before it is required

- 10: Get feedback before the report is locked

- How Presgo ESG Reporting Software Can Help

Singapore sustainability reporting has evolved from a ‘comply-or-explain’ approach to more rigorous and comprehensive climate disclosure. This shift is driven by the International Sustainability Standards Board (ISSB) standards, giving companies a common language for sustainability-related financial disclosure designed to give investors consistent and comparable information on sustainability risks.

This article covers ten steps for companies to achieve ISSB-aligned ESG reporting, from building a risk and opportunity system to running climate scenario analysis and setting defensible targets for assurance.

Why is Singapore adopting the ISSB Standards in sustainability reports?

Singapore is positioning itself as a trusted global financial centre in a decarbonising economy. Inconsistent sustainability data can challenge that position. The Monetary Authority of Singapore and SGX RegCo align with ISSB reporting because it gives investors a more refined view of how sustainability issues affect financing and long-term business prospects.

Manufacturers and property companies, for example, face carbon pricing, water stress, and supplier disruption, while their assets face flooding. These companies need to explain the financial risks and how they affect valuation, insurance and capital planning. For instance, the Development Bank of Singapore (DBS), which complies with ISSB reporting, invests billions in sustainable financing while cutting financed emissions and building out its nature-related risk framework.

While Singapore companies face overlapping reporting standards, from SGX sustainability reporting requirements to GRI and SASB, ISSB gives businesses a climate-related disclosure baseline for capital markets.

But, are Singapore companies ready for ISSB-aligned climate disclosure?

Singapore companies’ readiness wasn’t very promising in an Ernst & Young 2025 study, where only 32% of companies addressed all 11 TCFD recommendations, which aligned with the ISSB standards. For climate reporting in FY2024, only 14% of companies considered using ISSB, and the same percentage have reduction targets for all three scope emissions.

While this may seem far from ideal expectations, companies can prepare ahead. In August 2025, ACRA and SGX RegCo extended the timeline of requirements with an updated climate reporting roadmap. That extended window is an opportunity for Singapore companies to transition and build the infrastructure and internal systems that ISSB reporting actually requires. The 10 steps below lay out how to use that time well.

How to Prepare for Singapore Sustainability Reporting: 10 Steps for ISSB Compliance

The ten steps below take companies from gap check to an approved and published disclosure.

1. Understand the Singapore reporting obligations and your reporting gaps

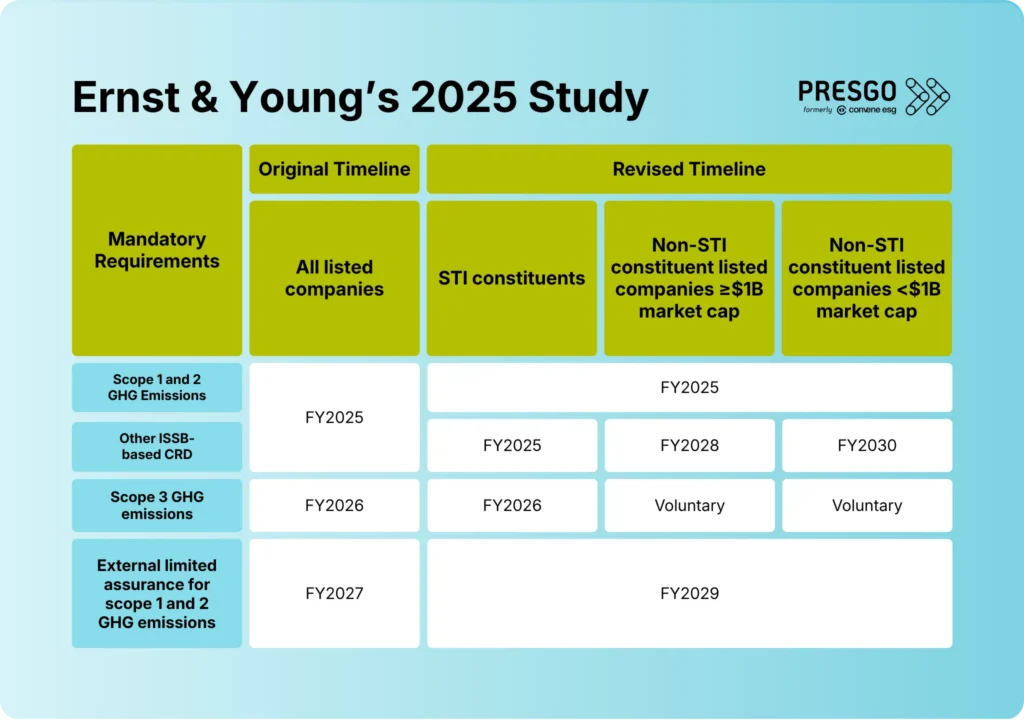

Before identifying risks or collecting data, companies must know exactly what the SGX and ACRA require. Under the updated August 2025 roadmap, SGX-listed users and STI- and non-STI-listed companies have varied phased requirements and timelines.

Source: ACRA Extended Timelines

- All listed companies: These companies must continue reporting scope 1 and scope 2 greenhouse gas (GHG) emissions from financial years starting on or after January 2025.

- STI companies: They are required to also report other ISSB-based climate-related disclosures from FY2025, followed by scope 3 emissions from FY2026.

- Non-STI listed companies with a market cap of S$1 billion and above: These companies must report other ISSB-based climate-related disclosures from FY2028.

- Non-STI listed companies with a market cap below S$1 billion: Companies under this category have to report other ISSB-based climate-related disclosures from FY2030.

For both non-STI listed companies, their scope 3 emissions reporting remains voluntary. The August 2025 update effectively gave non-STI companies an additional 2-5 years, depending on market cap, for climate-related disclosures and scope 1 and 2 external assurance.

Output: A confirmed timeline and IFRS S1 and S2 requirements that apply to the company.

2. Identify gaps and choose the right tools

This step is for companies to conduct a gap check before anything else, mapping what the company currently discloses against the specific requirements that apply. Once the gaps are identified, the next question is what system will support the entire work.

ESG reporting software is now used to centralise data collection and map disclosures to multiple frameworks and standards. Starting with the right tools early builds the data and materiality infrastructure that sustainability reporting requires.

For Singapore companies concerned about the cost of this technology, the Sustainability Reporting Grant (SRG) offers expense offsets. The grant supports SGX-listed companies to help build ISSB-aligned reporting capabilities, including the cost of consultant guidance and adopting ESG software.

Output: A compliance gap list specific to the IFRS reporting requirements, mapped against what the company currently has and what still needs building. Also, a list of tools needed to close each gap.

3. Identify material issues and create a materiality matrix

ISSB reporting starts with sustainability-related risks and opportunities before the reporting template itself.

Companies conduct materiality assessments to surface and evaluate material issues that impact all aspects of the company, including revenue, assets, liabilities, financing, and reputation. The SASB Standards Navigator can help in identifying sustainability issues to map them out in the next step. These issues can range from climate concerns and water security to workforce safety, supply chain labour practices, data governance, and resource use, depending on the sector. Each item should include the affected business unit, value chain link, potential financial impact, current owner, and time horizon (short-, medium-, or long-term).

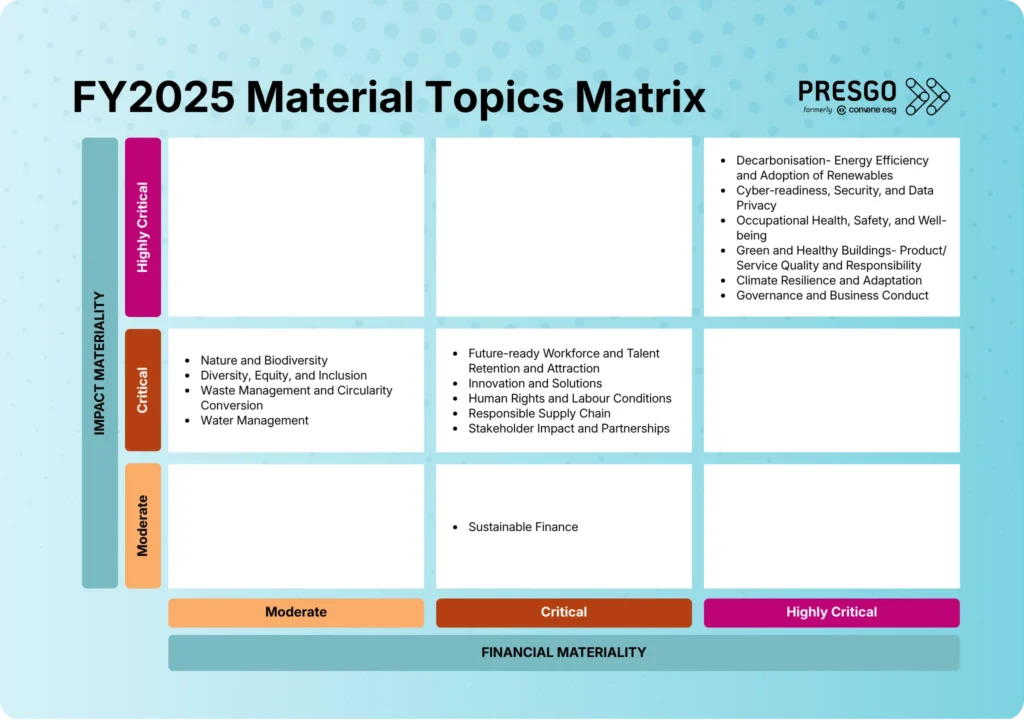

With the material topics already identified, they can then be plotted on a materiality matrix. This visual representation has two axes that measure the likelihood of the risk or opportunity affecting the business and the magnitude of the potential financial impact. This matrix process reveals that topics can be dependent on the company’s business model and shows where the company’s ESG efforts and priorities should be concentrated. Issues that score high on both axes are material and require full disclosure, while those that score too low on both can be set aside for monitoring.

An example of this step is a Singaporean global real estate company, City Developments Limited (CDL). CDL surveyed more than 425 stakeholders to rank 16 ESG issues across both impact and financial materiality dimensions. The resulting matrix aligns with the IFRS guide and classifies the material topics as moderate, critical, or highly critical.

Source: City Developments Limited 2026 Sustainability Report

Output: A signed-off materiality matrix with prioritised issues, each with a documented rationale.

4. Get leadership buy-in

A materiality matrix will not have as much impact without the visibility and support of the people who control the budget, strategy, and operations. This step is about converting the output of the first steps into internal alignment before the actual drafting of the report.

Finance and sustainability teams need to review the materiality matrix and present it to senior leadership and the board. The goal here is to confirm that the issues plotted as high-magnitude are actually reflected in how the company allocates capital, manages risk, and makes strategic decisions. As each material issue requires ownership, this process surfaces accountability gaps that assess the responsibilities of those beyond the company’s sustainability team. So, depending on how the management responds, the strategy and governance aspects in this step will show in the reporting.

Output: Leadership-validated responses to each material issue, with named owners, linked budget, and agreed strategic responses.

5. Run climate scenario analysis

IFRS standards, specifically the S2, expect companies to discuss climate resilience, usually through a scenario analysis. The work can be technical, but the logic is simple: test how the business performs under different climate futures.

Use at least two scenarios. One should reflect a lower-warming pathway, such as 1.5°C or below 2°C. Another should reflect a higher-warming pathway, such as 3°C or 4°C. The first tests transition pressure. The second tests physical risk.

A low-warming scenario may include higher carbon prices, tighter regulation, faster clean technology adoption, and changing customer demand. A high-warming scenario may include more heat stress, flooding, water stress, and supply chain disruption.

Output: A documented scenario analysis showing the financial direction of climate risks.

6. Build the emissions inventory and sustainability metrics

Companies can expect that the data work of collecting and analysing may take longer than the writing itself.

In this step, companies will benefit from starting an emissions inventory, documenting calculation methods, emission factors, assumptions, and data owners. This is a crucial step because for Singapore-listed companies, scope 1 and scope 2 emissions reporting is already mandatory from FY2025. STI-listed companies must add scope 3 from FY2026, while non-STI companies can treat scope 3 as voluntary for now. But even then, starting early is still a practical choice since scope 3 data takes years to build across a company’s supply chain.

Beyond emissions, SGX-listed companies must also report against core sustainability metrics. These metrics sit alongside the IFRS S1 requirement that management has to address. These are the material topics under the ESG pillars:

Environmental

- Greenhouse gas (GHG) emissions

- Energy consumption

- Water consumption

- Waste generation

Social

- Gender diversity

- Age-based diversity

- Employment

- Development and training

- Occupational health and safety

Governance

- Board composition

- Management diversity

- Ethical behaviour

- Certifications

- Alignment with frameworks

- assurance

Output: A complete emissions inventory across the required scopes and a set of metrics for each material sustainability topic, all with documentation and data owners.

7. Set ESG targets and policies

List current sustainability targets first. Include the baseline year, target year, scope, metric, and latest progress. For climate, be clear whether the target covers scope 1, scope 2, scope 3, or all three.

A weak target is easy to spot. Targets should connect to the company’s actions and results. Energy efficiency, renewable electricity, supplier engagement, fleet changes, process redesign, and product shifts should not sit in a separate strategy and should support the target. When targets, metrics, and operational plans work together, the strategy section of the ISSB report emerges from the evidence.

Output: A targets table with metric, baseline, goal, latest progress, and implementation actions for the Metrics and Targets pillar of ISSB reporting.

8. Structure the report around the four ISSB pillars

IFRS sustainability disclosure standards S1 and S2 follow the structure of governance, strategy, risk management, and metrics and targets.

- In the case of governance, companies should explain board oversight and management responsibility, avoiding vague claims when reporting.

- In strategy, companies must show the material risks and opportunities, explaining effects on the business model, value chain, financial planning, capital allocation, and climate scenario analysis.

- In risk management, companies should describe how risks are identified, assessed, prioritised, and monitored.

- In metrics and targets, presenting the numbers includes GHG emissions, material metrics, baselines, targets, and methods.

This structure keeps the ISSB report readable and makes gaps harder to miss.

Output: A complete draft ISSB report structured around the four pillars, with every material issue from steps 2 to 7 mapped out to its appropriate section.

9. Prepare for assurance before it is required

Companies build a long-term process by tagging every figure that may later be assured and keeping source files and supporting evidence for each. Then a second-person check, review, and department sign-off can catch many errors before the ISSB report is published.

With Singapore’s assurance timeline, companies have enough breathing space and allowance to fully prepare. Limited external assurance on scope 1 and scope 2 emissions is required from FY 2029 for all SGX-listed companies. Large non-listed companies will follow from FY 2032. Companies that wait until FY2028 to start will fall behind. It takes multiple reporting cycles to fully embed the data infrastructure and reporting discipline required for limited assurance.

Output: An assurance-ready data package, complete with source files, calculation notes, approval records, and a documented gap list that must be strengthened before the FY deadline.

10: Get feedback before the report is locked

ISSB reporting is investor-focused, but investors are not the only ones who can be useful reviewers. A near-final draft should be tested with the board, finance team, assurance providers, and other selected stakeholders. Feedback should be logged for documentation, as it will be useful for evaluation and future information to improve the current report. This loop will continue to matter because sustainability reporting standards will continue to develop, and regulations will continue to tighten.

Output: A reviewed, board-approved final report, with a documented feedback log and a list of improvements carried into the next reporting cycle.

How Presgo ESG Reporting Software Can Help

The ISSB sustainability reporting will expose weak data systems quickly. A simple spreadsheet will not hold up when teams need audit trails, seamless workflow, evidence files, supplier data, and reports aligned with other frameworks.

Presgo’s ESG reporting solutions are built for that problem. Presgo is an AI-first, modular ESG software for data collection, carbon accounting, disclosure management, and report generation. It supports global frameworks such as GRI, SASB, TCFD, and ISSB standards, along with local requirements, including SGX and other market rules.

It gives sustainability, finance, and risk teams a cleaner system to work from. For companies preparing for the Singapore sustainability reporting, that may be the difference between rushed compliance and a report that holds up under investor, regulator, and assurance review.

Book a demo today and take control of your ISSB-aligned reporting in 2026.