Talk to an ESG Expert about how Presgo can help you!

Our ESG Experts are on-hand to understand your ESG Reporting needs and cater our solution to you. Get in touch to discuss how we can help.

Talk to an ESG ExpertContents

- What is the National Sustainability Reporting Framework (NSRF)?

- Who needs to comply with the NSRF?

- What is the timeline for NSRF implementation?

- What are the requirements of the NSRF?

- What are the proportionality mechanisms and additional transition reliefs?

- How to Start Sustainability Reporting Under the NSRF

- What are the challenges in adopting the NSRF?

- Why is the NSRF important?

- How Presgo Supports NSRF Reporting

NSRF Malaysia is the country’s mandatory ESG disclosure regime, adopting IFRS S1 and S2 as its national baseline standards. Spearheaded by the Securities Commission Malaysia, it transitions corporate reporting from voluntary TCFD adoption to compulsory IFRS Sustainability Disclosure Standards. Below is a guide to the NSRF, its implementation timeline, and how Malaysian companies can comply.

What is the National Sustainability Reporting Framework (NSRF)?

The National Sustainability Reporting Framework (NSRF) is Malaysia’s official regulatory framework that makes IFRS Sustainability Disclosure Standards, often referred to as ISSB Standards, mandatory for companies. Issued on September 24, 2024, by the Securities Commission Malaysia, it transitions Malaysia from voluntary TCFD-based reporting to compulsory, globally aligned ESG disclosure. With the introduction of the NSRF, Malaysia joins over 20 jurisdictions adopting ISSB Standards.

The establishment of the NSRF mandates IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and S2 (Climate-related Disclosures) as the baseline for all companies. NSRF Malaysia’s governance is overseen by the Advisory Committee on Sustainability Reporting (ACSR), an inter-agency body that includes SC Malaysia, Bank Negara Malaysia, Companies Commission of Malaysia, Bursa Malaysia, Audit Oversight Board, and Financial Reporting Foundation.

The NSRF aims to standardize corporate sustainability reporting by aligning local disclosures with existing global frameworks. This ensures that applicable companies provide consistent, comparable, and reliable ESG data to attract foreign investors and remain competitive.

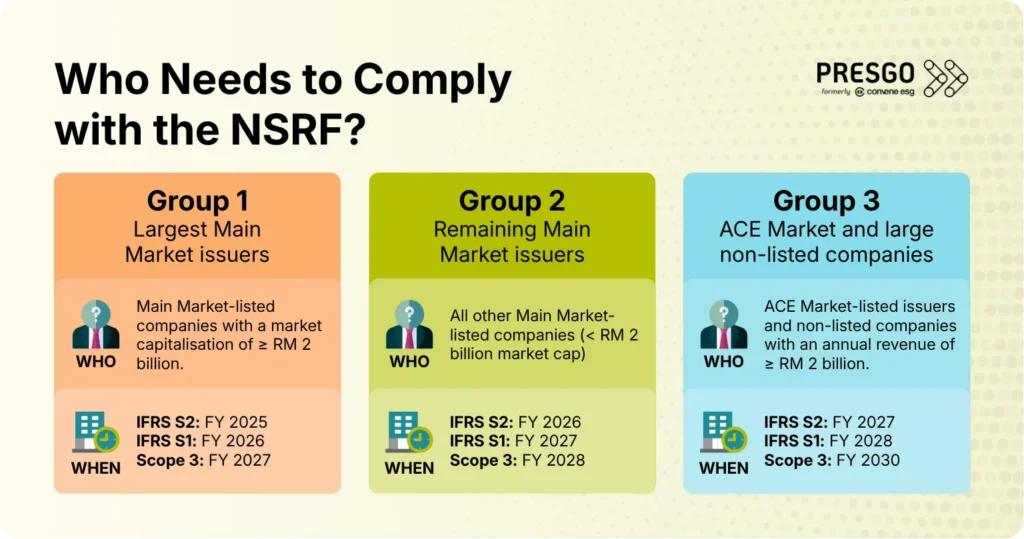

Who needs to comply with the NSRF?

The NSRF applies to listed issuers and large non-listed companies in Malaysia. These are divided into three groups based on their size, with larger companies reporting first:

Group 1: Largest Main Market issuers

Who: Main Market-listed companies with a market capitalisation of RM 2 billion or higher.

When: IFRS S2 (climate-related disclosures) started in FY 2025, while IFRS S1 (all material sustainability-related risks and opportunities) starts in FY 2026, and scope 3 emissions reporting starts in FY 2027.

Group 2: Remaining Main Market issuers

Who: All other Main Market-listed companies (below RM 2 billion market cap).

When: IFRS S2 starts in FY 2026, IFRS S1 starts in FY 2027, and scope 3 starts in FY 2028.

Group 3: ACE Market and large non-listed companies

Who: ACE Market-listed issuers and non-listed companies with an annual revenue of RM 2 billion or higher.

When: IFRS S2 starts in FY 2027, IFRS S1 starts in FY 2028, and scope 3 starts in FY 2030.

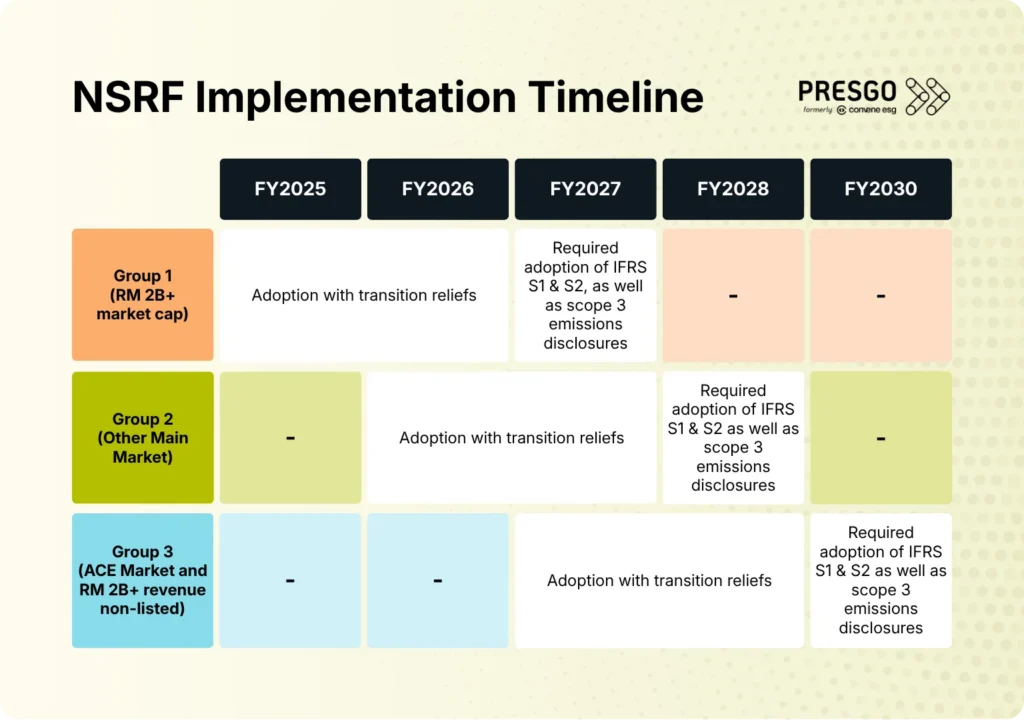

What is the timeline for NSRF implementation?

The NSRF uses a phased implementation timeline from 2025 to 2030, with climate reporting (IFRS S2) starting first, followed by all material sustainability-related risks and opportunities (IFRS S1), then scope 3 emissions. The reporting requirements also include additional transition reliefs and exemptions. This phased approach allows companies to build capacity, with larger or more mature companies reporting first.

Below is the implementation timeline for each group of applicable entities:

What are the requirements of the NSRF?

The NSRF requires Malaysian companies to comply with IFRS S1 and S2 standards, with specific disclosure requirements organised around the four TCFD pillars: Governance, Strategy, Risk Management, and Metrics & Targets, where the ISSB Standards are heavily relied upon.

Climate-first reporting (IFRS S2)

Companies must start with climate disclosures, which include:

- Governance: Board oversight of climate risks or opportunities, and management’s role in assessing climate issues

- Strategy: Climate-related risks and opportunities, their impact on business model and financials, and scenario analysis

- Risk Management: How climate risks are identified, assessed, managed, and integrated into overall risk management

- Metrics & Targets: Scopes 1 and 2 emissions, climate targets, and industry-specific metrics

When climate reporting has been established, companies are then required to expand to broader sustainability topics, such as:

- Labour practices and human rights

- Biodiversity and ecosystem impacts

- Supply chain risks

- Water and resource management

- Other material sustainability-related risks and opportunities, determined in their materiality assessments

Emissions reporting requirements

Scopes 1 & 2:

- Required from the start for all groups

Scope 3:

- Group 1: FY 2027, Group 2: FY 2028, and Group 3: FY 2030

General reporting requirements

Companies must meet these practical reporting obligations:

- Reports must be included in the annual report and filed in XBRL format via the Bursa Malaysia or the SSM portal

- Board-level approval required for all disclosures

- Limited assurance expected within 2 reporting cycles

- Disclosures must be connected to financial statements, not treated as separate exercises

What are the proportionality mechanisms and additional transition reliefs?

The NSRF includes both built-in proportionality mechanisms (from IFRS S1/S2) and additional transition reliefs specifically added by Malaysia to ease adoption.

Proportionality Mechanisms

These are embedded in IFRS S1 and S2 to help companies with different capabilities apply the standards:

- All reasonable and supportable information

- Companies only need to use information available at the reporting date without undue cost or effort

- Commensurate with skills, capabilities, and resources

- Disclosures should match the company’s available skills, capabilities, and resources

- No quantitative information exemption

- If quantitative data isn’t available, companies must provide qualitative information and explain why quantitative information isn’t provided

- No exemptions from disclosure

- Mechanisms don’t introduce new requirements or exempt companies; they adjust how requirements are applied based on capability

These mechanisms address challenges related to data constraints and availability without compromising the quality of decision-useful information for investors.

Additional Transition Reliefs

The NSRF provides these Malaysia-specific reliefs to support a smoother transition:

- Climate-first approach

- Focus on climate-related disclosures first (IFRS S2)

- Broader ESG topics (IFRS S1) deferred to the second reporting year

- Additional time for complex reporting

- Groups 1 &2 are given extra time not to report scope 3 emissions for the first two annual reporting periods, whereas Group 3 is permitted not to report for the first three annual reporting periods.

- Comparative information relief (ISSB relief)

- In the first year of reporting, companies don’t need to provide comparative information from the prior year

- Parent company reliance

- Companies can rely on parent company reports if they align with ISSB or ESRS standards

- Flexible measurement approach

- Relief from using the GHG Protocol if currently using a different emission measurement approach

These reliefs allow companies to report sustainability and climate-related disclosures at a manageable pace, supporting the NSRF’s phased and developmental approach.

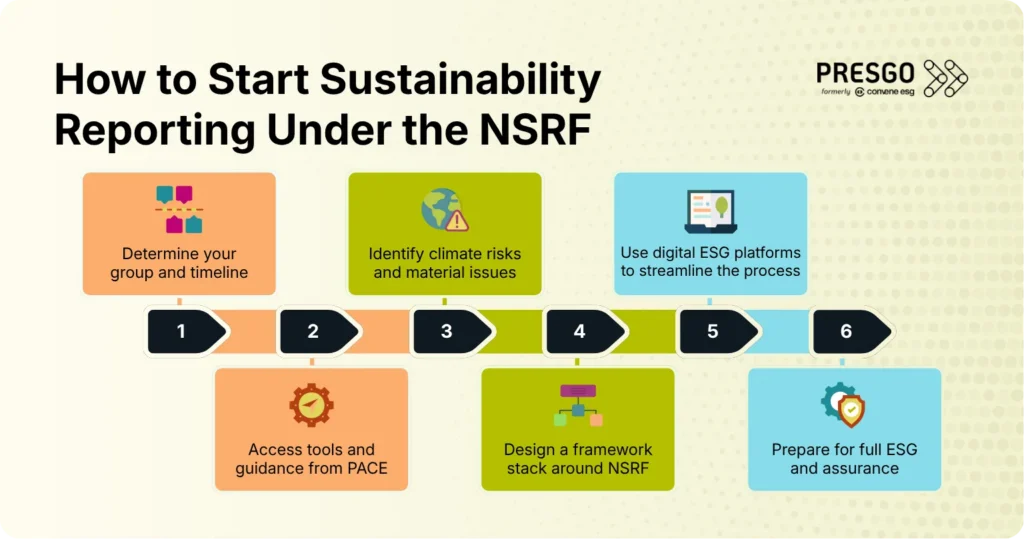

How to Start Sustainability Reporting Under the NSRF

Organisations can start sustainability reporting under the NSRF by following a structured, phased approach that gradually builds their capacity. Below are crucial steps for companies to follow:

- Determine your group and timeline

First, identify which group your organisation belongs to in order to know your reporting deadlines:

- Group 1: Main Market

- Group 2: Other Main Market issuers

- Group 3: ACE Market and non-listed companies

- Access tools and guidance from PACE

Use the PACE Hub (Policy, Assumptions, Calculators, and Education), which provides policy guidance, emissions calculators, capacity-building programmes, and resources designed to help companies comply with the NSRF. Companies can also use ESG reporting tools to support framework-aligned sustainability reports. PACE offers:

- Policy: Practical guidance on sustainability policies and how they align with business strategies, ensuring compliance with NSRF and international standards for Main Market, ACE Market, and large non-listed companies

- Assumptions: Standardised assumptions and methodologies for emissions calculations to ensure accuracy and comparability across companies

- Calculators: Emissions calculators for measuring scopes 1-3 greenhouse gas emissions, simplifying carbon footprint measurement while meeting NSRF requirements

- Education: Capacity-building programs, including workshops, training sessions, and educational materials, to upskill ESG teams on ISSB standards

- Identify climate risks and material issues

Follow the NSRF’s practical steps for initiating reporting:

- Strategic planning to collect and report sustainability data

- Pinpoint what matters for your industry and stakeholders, e.g., materiality assessment

- Begin with scopes 1 and 2 emissions, and report across the four TCFD pillars. Include scenario analysis for climate-related risks as part of your climate disclosures.

- Design a framework stack around NSRF

Master relevant frameworks such as GRI, IFRS, and Bursa Malaysia requirements. While the NSRF sets IFRS S1 & S2 as the baseline sustainability disclosure standards in Malaysia, other frameworks such as the GRI and Bursa Malaysia’s Sustainability Reporting Guide can help deepen report content and clarify expectations.

- Use digital ESG platforms to streamline the process

Modern ESG platforms can help ensure compliance and comparability while enhancing risk management by integrating climate and sustainability into overall risk frameworks. Regardless of size, ESG teams can rely on these platforms for accurate data collection and automated report generation.

- Prepare for full ESG and assurance

In the second reporting year, expand to IFRS S1 covering labour, biodiversity, supply chain, and other material sustainability topics. Prepare for limited assurance within two reporting cycles, and ensure disclosures are included in your annual report and filed in XBRL format via the Bursa Malaysia or SSM portal.

What are the challenges in adopting the NSRF?

Adopting the NSRF presents several challenges for companies, particularly given the varying levels of maturity in sustainability practices across organisations:

System and Data Infrastructure

One of the main challenges is adapting existing information and reporting systems to the new IFRS S1 and S2 requirements, which can require significant investment in technology and labour. Companies face data gaps in tracking emissions, especially scope 3 emissions, which require supply chain data that many organisations don’t currently collect.

Integration with Business Strategy

Companies must navigate the complexity of integrating sustainability and climate considerations into their commercial strategies and operations, which is a time and resource-consuming process. This goes beyond simple compliance, as it requires embedding sustainability into core business decision-making.

Quantifying and Measuring Impact

The medium and long-term effects of climate risks are difficult to assess quantitatively, given that there isn’t always a direct relationship between climate-related risks and financial position. It can be challenging to distinguish climate-related effects from other effects on an entity’s financial position, which impacts the reliability of information.

Scenario Analysis and Comparability

Determining which scenarios to use for climate scenario analysis can be challenging, as scenarios chosen by different entities may not be consistent or comparable between companies. Investors are most interested in the sensitivity analysis of key parameters rather than the scenarios themselves, but achieving comparability requires globally recognised external scenarios.

Talent and Expertise Shortages

There are talent shortages in ESG reporting expertise, particularly for finance leaders who need to understand IFRS standards while also managing climate risk identification and scenario analysis. Companies need to build internal capacity through training programmes like those offered under PACE.

Why is the NSRF important?

The NSRF transforms ESG reporting in Malaysia from voluntary to mandatory, aligning the country with global standards and driving tangible business and economic outcomes. Key reasons that the NSRF is important include:

Global alignment and competitiveness

NSRF Malaysia positions the country alongside over 20 jurisdictions representing 55% of the global GDP that have adopted IFRS S1 and S2. As a major trading nation, this early adoption gives Malaysia a competitive advantage and attracts foreign investment. International investors demand consistent, comparable sustainability data, which the NSRF delivers through mandatory IFRS-based disclosures.

Climate action and net-zero goals

The NSRF’s climate-first approach prioritizes IFRS S2 reporting, directly supporting Malaysia’s net-zero targets with transparency. The country has pledged to reduce emissions intensity to achieve net-zero as early as 2050. Companies must report climate risks and opportunities, enabling informed sustainability decisions. Linking sustainability disclosures to financial reporting improves information quality for investors.

Market integrity and investor protection

The NSRF makes ESG reporting mandatory through enforceable IFRS S1 and S2 compliance. Non-compliance results in fines, administrative action, delisting risks, and reputational harm for companies. Limited assurance for scopes 1 and 2 emissions will start by 2027, improving data quality.

Business resilience and capacity building

The NSRF’s phased approach lets companies implement sustainability reporting gradually based on their size and readiness. Transition reliefs like extra time for scope 3 emissions and reliance on parent company reports make adoption manageable. Capacity-building support is available through initiatives like the PACE Hub.

Economic and strategic value

The NSRF enhances Malaysia’s attractiveness to investors by providing reliable, standardised sustainability information. It was developed through extensive stakeholder consultation to meet actual market needs. The framework ensures Malaysian companies remain competitive, where sustainability disclosure is essential for capital access.

How Presgo Supports NSRF Reporting

Malaysian companies can make use of modern ESG reporting tools to support NSRF-based reporting. The framework requires complex data collection, calculation, and management of scopes 1 to 3 emissions across supply chains, which manual systems cannot handle efficiently.

This is where Presgo comes in. The AI-first ESG reporting platform aligns ESG reporting with IFRS S1 and S2 standards, which are the core standards mandated by Malaysia’s NSRF. Teams can also use the platform’s flexible reporting templates along with best practice recommendations from experts to define report scope and guarantee full compliance with the NSRF.

Prepare for sustainability reporting under the NSRF and book a demo with Presgo today!