-

AI-First ESG Reporting

Start your ESG journey today with Presgo

Talk to an ESG Expert

Task Force on Climate-Related Financial Disclosures (TCFD) Reporting

The Task Force on Climate-Related Financial Disclosures (TCFD) is a global framework that standardises how companies report climate risks, opportunities, and their financial impacts. Created by the Financial Stability Board in 2015, it guides organisations in disclosing governance, strategy, risk management, and metrics related to climate issues, enabling investors to assess resilience and long-term value. Many APAC regulators now base upcoming sustainability reporting rules on TCFD, making it a core reference for credible, decision-useful ESG reporting.

Book a Personalised Meeting Today!

"*" indicates required fields

Talk to an ESG Expert about how Presgo can help you!

Our ESG Experts are on-hand to understand your ESG Reporting needs and cater our solution to you. Get in touch to discuss how we can help.

What is TCFD?

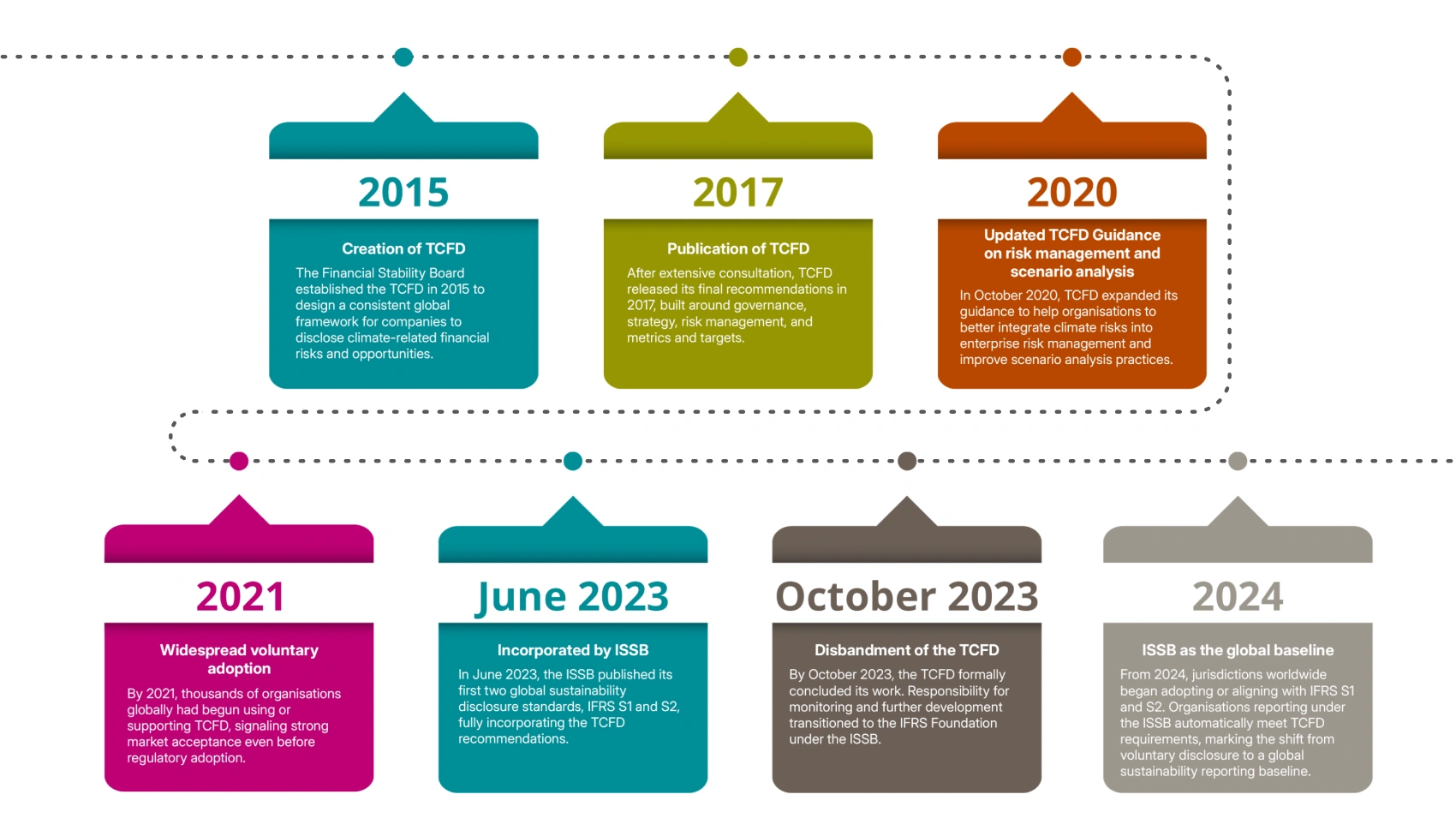

Climate change poses financial risks to businesses and the global economy. In 2015, the Financial Stability Board (FSB) established the Task Force on Climate-related Financial Disclosures (TCFD) to define best practices on how companies should report climate-related risks, opportunities, and emissions to investors, lenders, and insurers.

Over several years of consultation, TCFD’s recommendations have become widely accepted globally, used by many companies voluntarily for their ESG reports.

In 2023, the FSB declared that the TCFD had fulfilled its remit and officially disbanded. Responsibility for global climate-related financial disclosures is now carried over to the International Sustainability Standards Board (ISSB) under the IFRS Foundation. The inaugural ISSB standards (IFRS S1 and IFRS S2) fully incorporate the TCFD recommendations.

Companies may continue to reference TCFD directly if they choose, but moving forward, ISSB standards will serve as the global baseline for corporate climate-related disclosure.

What is the TCFD framework?

In October 2021, the Task Force updated its Guidance that supersedes the 2017 Annex, adding more recommended disclosures. Developing the standardised framework for climate reporting, the Task Force defined categories for climate-related risks and opportunities. This classification should serve as a guide for organisations to assess and disclose the matters that are pertinent to their business operations.

For the climate-related risks, TCFD has segmented them into two categories: (a) risks related to the transition to a lower-carbon economy, and (b) risks related to the physical impacts of climate change. For climate-related opportunities, these may vary according to the region, market, and sector in which the organisation operates. To create a cohesive report, the Task Force encourages accompanying the risks and opportunities with the potential financial impact.

The TCFD recommendations are structured around four thematic areas: Governance, strategy, risk management, and metrics and targets. These core elements are supported by recommended disclosures that set out what information companies must disclose.

What are the TCFD recommendations?

Governance

Disclose the organization’s governance around climate- related risks and opportunities.

- Recommended Disclosures

- Describe the board’s oversight of climate related risks and opportunities.

- Describe management’s role in assessing and managing climate-related risks and opportunities.

Strategy

Disclose the actual and potential impacts of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning where such information is material.

- Recommended Disclosures

- Describe the climate-related risks and opportunities the organization has identified over the short, medium, and long term.

- Describe the impact of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning.

- Describe the resilience of the organization’s strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario.

Risk Management

Disclose how the organization identifies, assesses, and manages climate-related risks.

- Recommended Disclosures

- Describe the organization’s processes for identifying and assessing climate- related risks.

- Describe the organization’s processes for managing climate-related risks.

- Describe how processes for identifying, assessing, and managing climate-related risks are integrated into the organization’s overall risk management.

Metrics and Targets

Disclose the metrics and targets used to assess and manage relevant climate-related risks and opportunities where such information is material.

- Recommended Disclosures

- Disclose the metrics used by the organization to assess climate-related risks and opportunities in line with its strategy and risk management process.

- Disclose Scope 1, Scope 2, and, if appropriate, Scope 3 greenhouse gas (GHG) emissions, and the related risks.

- Describe the targets used by the organization to manage climate-related risks and opportunities and performance against targets.

What is a TCFD scenario analysis?

A TCFD scenario analysis is a critical tool to identify an organisation’s climate-related risks and opportunities aligned with the framework. By evaluating different climate scenarios, companies can anticipate a range of futures and develop strategies to mitigate risks and seize opportunities.

This forward-looking approach, emphasised by the TCFD framework, helps companies align their business models with a climate-resilient future, ensuring they are prepared for the challenges and opportunities ahead.

Below are the six steps for applying scenario analysis to climate-related risks and opportunities:

- Establish governance: Embed scenario analysis into strategic planning and/or enterprise risk management. Assign board-level oversight and clarify roles for internal and external stakeholders involved in the process.

- Assess climate materiality: Identify current and future climate-related risks and opportunities facing the organisation. Assess whether these exposures could become material and whether they are relevant to key stakeholders.

- Define scenarios: Select a credible range of climate scenarios aligned with identified exposures. Set clear assumptions, inputs, and analytical choices, including relevant reference or benchmark scenarios.

- Analyse business impacts: Evaluate how each scenario could affect strategy, operations, and financial performance. Identify critical drivers, thresholds, and sensitivities across the business.

- Identify strategic responses: Use scenario outcomes to inform practical risk and opportunity responses. Assess required changes to strategy, capital allocation, or financial planning.

- Document and disclose: Maintain clear documentation of methods, assumptions, and results. Communicate findings internally and prepare to disclose key inputs, outputs, and management responses externally.

What is the TCFD framework’s historical timeline?

The TCFD and ESG Reporting Frameworks and Standards

Integrating the TCFD recommendations or ISSB standards with existing reporting frameworks can streamline the process and enhance the quality of climate-related disclosures. Some of the frameworks and standards to integrate with TCFD or ISSB are:

CDP

The Carbon Disclosure Project (CDP) is a widely recognised framework for reporting environmental impacts. Companies can align their TCFD disclosures with CDP by mapping TCFD’s climate-related risk and opportunity categories to CDP’s detailed questionnaires. This alignment not only simplifies reporting but also ensures consistency across various disclosures, enhancing the comparability and reliability of climate-related information.

SASB

The Sustainability Accounting Standards Board (SASB) provides industry-specific standards that focus on financially material sustainability issues. Companies can leverage SASB’s sector-specific guidance to align their TCFD disclosures, particularly when identifying and reporting on material climate-related risks and opportunities. This approach allows companies to deliver more targeted and relevant information to investors.

UN SDGs

The United Nations Sustainable Development Goals (UN SDGs) provide a global framework for addressing interconnected social, economic, and environmental challenges, including climate action. Companies can align their TCFD disclosures with the UN SDGs by mapping climate-related risks and opportunities to relevant goals, such as SDG 13 (Climate Action) and SDG 7 (Affordable and Clean Energy).

Explore the rest of the ESG frameworks and standards supported by Presgo.

Who needs to comply with the TCFD framework?

The IFRS Foundation notes that an increasing number of countries are integrating ISSB Standards, which incorporate TCFD, into mandatory reporting regimes for listed companies. Below are some of the stakeholders required to comply with the framework:

Corporations

Companies across sectors are increasingly adopting TCFD recommendations to demonstrate their commitment to addressing climate risks, ensuring they meet investor expectations and regulatory requirements.

Financial Sectors

Banks, insurers, and asset managers use TCFD-aligned information to evaluate the climate risks in their portfolios, ensuring that their investments are resilient to climate change impacts. Financial institutions also typically pair TCFD with SASB, adding financial materiality for more comprehensive climate risk disclosures.

Non-Financial Sectors

Sectors such as Energy, Materials and Buildings, Transportation, and Agriculture face detailed supplementary recommendations from the TCFD. These typically include high-emission and capital-intensive activities vulnerable to physical and transition risks. For entities in non-financial sectors, the TCFD is often combined with frameworks such as CDP, GRI, and SASB. For example, mining companies use CDP for a more detailed look at climate data and supply chain impacts, while energy companies may combine TCFD with GRI and SASB for more stakeholder and industry-specific focus.

How Presgo Supports TCFD-Aligned Disclosures

Presgo is an AI-first ESG reporting platform designed to streamline compliance with frameworks like TCFD. Using integrated modules that automate data collection, analysis, and disclosure generation, the platform supports TCFD’s core pillars: governance, strategy, risk management, and metrics and targets.

Data Hub

Presgo’s Data Hub centralises ESG data from multiple sources, enabling seamless mapping to TCFD requirements for consistent climate risk reporting. It ensures audit-ready traceability across Scopes 1, 2, and 3 emissions and other metrics, thereby reducing manual errors in disclosures.

Disclosure Hub

Disclosure Hub helps automate TCFD-aligned report creation with a built-in framework mapping to standards, like ISSB, GRI, and CSRD. Users generate customisable, compliant reports that efficiently highlight climate-related risks, opportunities, and scenario analyses.

Carbon Calculator

The platform’s integrated Carbon Calculator computes Scopes 1, 2, and 3 emissions using verified factors from GHG Protocol and others, directly supporting TCFD’s metrics and targets pillar. AI-driven anomaly detection and transparent calculations deliver actionable insights for transition plans.

Materiality Assessment

The Materiality Assessment tool evaluates climate risks via double materiality, producing heatmaps aligned with TCFD’s strategy and risk management needs. It identifies financially material issues with stakeholder input, ensuring forward-looking disclosures.

Learn more about how you can create TCFD-aligned reports using Presgo.