Contents

- What are the sustainability reporting requirements in France?

- What is an ESG checklist?

- What to Consider When Creating an ESG Checklist

- What are the key components of an ESG checklist for French ESG reporting?

- How to Use the ESG Checklist Template

- FAQs on ESG Checklists

- Fast-track Your ESG Report Checklist with Presgo

Sustainability reporting regulations are evolving fast. In the European Union, reporting directives have been amended, leading to many proposed revisions. And yet, part of these rapid developments is the demand for companies to keep up with the pace while staying competitive and profitable.

France, as part of the EU, has been moving decisively in navigating these sustainability frameworks early. It has been considered a pioneer in sustainability, as the country was a major facilitator of the Paris Agreement and the first EU country to implement the CSRD into national law.

For French companies already facing pressure from stakeholders, the dynamicity creates both a burden and an opportunity. How then should companies in France organise their processes to deliver ESG reports?

In this article, we’ll be discovering how to build a step-by-step ESG checklist for ESG reporting, and how France began with sustainability disclosures.

What are the sustainability reporting requirements in France?

Before and outside the Paris Agreement in 2015, France had been actively pushing for ethical practices in the early 2000s. The country then made more major revamps after ratifying the agreement.

Early Developments: NRE and Grenelle II Laws

France’s early step was the introduction of the Nouvelles Régulations Économiques (NRE) or the New Economic Regulations law in 2001. It required companies listed on the Paris Stock Exchange to add the ‘ethical’ aspect in their annual reports, later known as disclosing social and environmental data.

Building on this foundation, the Grenelle II Law of 2010 expanded sustainability reporting obligations. It extended the scope to non-listed companies and introduced third-party verification and required greenhouse gas (GHG) emissions reporting. The law also formalised the use of the Bilan Carbone, a carbon reporting method developed in 2004, as a mandatory reporting requirement in France.

The Declaration of Extra-Financial Performance

In 2017, France went beyond environmental issues and introduced the Déclaration de Performance Extra-Financière (DPEF). It was under the transposition of the EU Non-Financial Reporting Directive (NFRD), through France’s Ordonnance n° 2017-1180 and Décret n° 2017-1265. Its mechanisms also replaced those of the Grenelle II Law, requiring certain large companies to publish information on ESG issues in their annual management reports.

- Scope: Applied mainly to large listed companies and certain unlisted companies that exceed their identified thresholds (500 employees, €100M turnover or €100M balance sheet).

- Content Requirements: Disclosures on ESG issues, such as environmental matters, social and employee-related issues, respect for human rights, and anti-corruption efforts.

- Format and Flexibility: Companies had the flexibility to choose their reporting framework, like the Global Reporting Initiative (GRI), leading to scope and quality variations.

Complementary National Developments

Alongside the DPEF, France continues to reinforce its national sustainability reporting framework. To push for transparency, the country formed these domestic policies for corporate responsibility reporting.

- French Commercial Code: Established the legal foundation for non-financial reporting, requiring large companies to disclose key environmental, social, and governance information.

- Article 173 of the Energy Transition Law: A parallel disclosure law that required institutional investors to report on how they manage climate-related and carbon risks.

- Loi PACTE 2019: Broadened corporate governance by encouraging companies to incorporate social and environmental considerations into their long-term strategies.

Corporate Sustainability Reporting Directive

With DPEF’s scope and comparability limitations, the need for hard data to fully assess risks and opportunities led them to the Corporate Sustainability Reporting Directive (CSRD). France was among the first EU states to incorporate the CSRD into national adoption in 2023, replacing the DPEF entirely.

What were the major developments from DPEF to CSRD?

CSRD builds on the lessons learnt from DPEF while introducing stricter, more harmonious, and enforceable requirements. Here are the major differences between France’s DPEF and the developments in the country’s CSRD implementation:

| Aspect | DPEF | CSRD |

| Scope | Large listed companies and particular unlisted companies that exceed their identified thresholds (500 employees, €100M turnover or €100M balance sheet) | Extended to 50,000 EU companies, including listed SMEs and non-EU entities with EU activity |

| Reporting Standards | No standardised format, focusing on flexibility over consistent scope and quality of disclosures | Mandatory use of the European Sustainability Reporting Standards (ESRS) |

| Materiality | Single materiality (impact on the company) | Double materiality (impact on and by the company) |

| Assurance | Limited external verification | Mandatory limited assurance by accredited ESG auditors |

| Digital Format | Paper/PDF narrative disclosure | Digital tagging (xHTML and XBRL taxonomy) for EU comparability |

The developments from the DPEF and CSRD can be a learning curve. Under the CSRD’s double materiality rule, French companies must include in their ESRS-compliant report both their sustainability impacts and how sustainability issues affect their business.

The shift from DPEF to CSRD also introduces a more complex process for ESG reporting. It now requires deeper integration of data and broader disclosure across the ESG pillars. French companies must adopt clear processes and practical tools, like step-by-step ESG checklists, to navigate these regulatory requirements and deliver a reliable ESG report annually.

What is an ESG checklist?

An ESG checklist is a structured tool that guides ESG reporting and performance with mapped-out points or questions, based on regulations, standards, and framework audit requirements. Considered as a foundational template for ESG compliance, it bridges a high-level strategy to the gritty work of gathering numbers, narratives, and ESG audit support.

For French companies, a well-constructed ESG checklist can help teams translate reporting requirements into concrete and workable tasks and components.

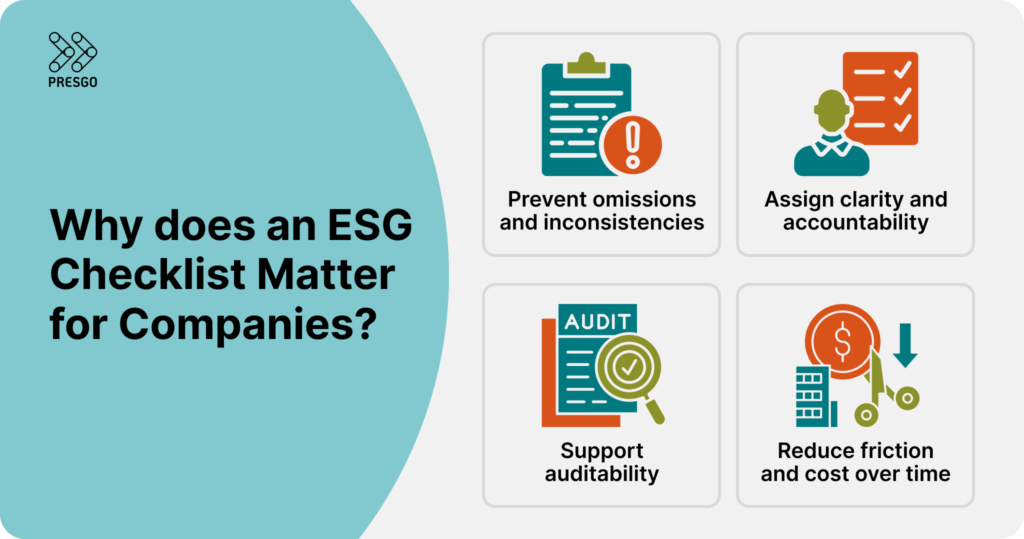

Why does an ESG checklist matter for companies?

An ESG checklist is not a requirement, but formalising the ESG process through this tool carries advantages for companies. Think of it as a project governance backbone for companies.

These are what companies can benefit from ESG checklists:

Prevent omissions and inconsistencies

ESG frameworks contain dozens of disclosure requirements. A checklist helps you reliably compare your draft report with those requirements.

Assign clarity and accountability

When each data point is paired with an owner, timeline, and review step, responsibilities are structured, and roadblocks are easily traceable for improvement.

Support auditability

Because assurance is mandatory, auditors will ask for proofs, controls, change logs, and rationales. A checklist that tracks all review gates or audit checkpoints becomes supporting documentation.

Reduce friction and cost over time

In the first few cycles, many tasks will be new or uncertain. A checklist helps you learn, refine, and stabilise the process so each subsequent year is more seamless.

What to Consider When Creating an ESG Checklist

Before a company can delve into the components and the detailed aspects, it must establish an ESG checklist that fits the company and the French rules. Some things to be considered are:

Who creates the ESG checklists?

Typically led by the ESG Reporting Team or Sustainability Department, with input from Finance, Legal/Compliance, HR, Operations, and IT. Corporate communications often helps with wording and publication. The diversity and collaboration of these departments will affect the whole process from creating to accomplishing the ESG checklist.

Are checklists publicly available?

You can find sample checklists from consulting firms and ESG software providers, but most companies build their own. Public templates can be used as starting points, but they still need tailoring to the company’s scope, data systems, and ESRS disclosures under the CSRD.

What does it cover?

It gathers and lists down tasks, timelines, data sources, and responsible teams across the full ESG reporting cycle. For each key component in the ESG checklist, there are different scopes covered and different bodies responsible for the creation and completion of an ESG report.

How is it structured?

An ESG checklist is a clear step-by-step framework that links data, actions, evidence, stakeholders, timelines, and progress tracking. It is broken down into different components, each wth its own finer details involved.

What are the key components of an ESG checklist for French ESG reporting?

For effective internal management, companies should set deadlines, establish review points, and assign a person or department responsible for each task. Below is an outline of the ESG reporting process, from planning to publication.

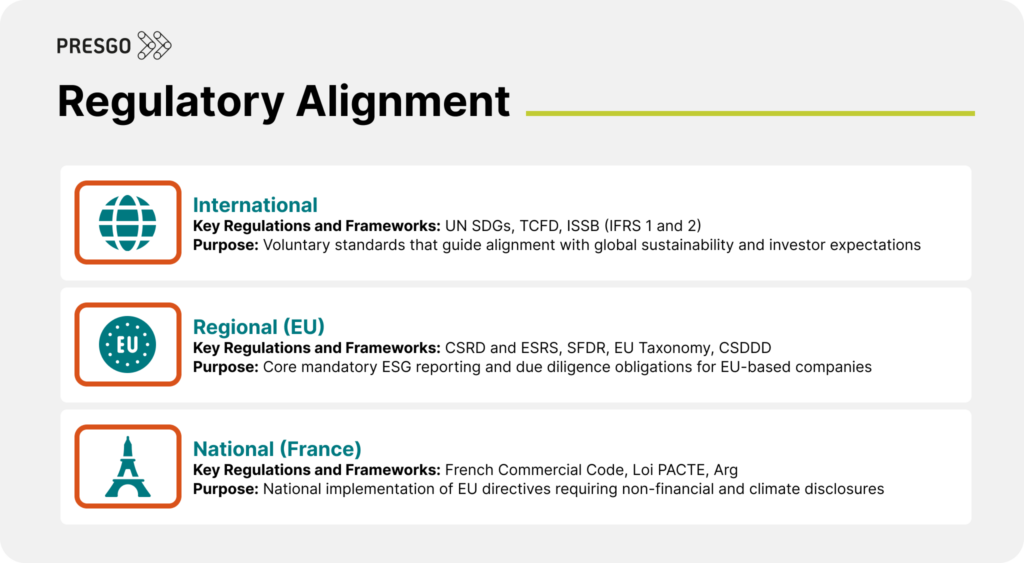

1. Regulatory Alignment

One component that is essential to include in the checklist is the latest reporting requirements. Teams should be updated on the ESG frameworks that apply in France and across the EU. These include the CSRD, the Sustainable Finance Disclosure Regulation (SFDR), and the EU Taxonomy for sustainable activities. An example of this in practice is L’Oréal’s sustainability report, which follows the CSRD standards and has a well-established reporting system.

To support this alignment, the table below provides a high-level checklist of key regulations and frameworks that French companies should consider to help teams identify which frameworks are most relevant to their operations and timelines.

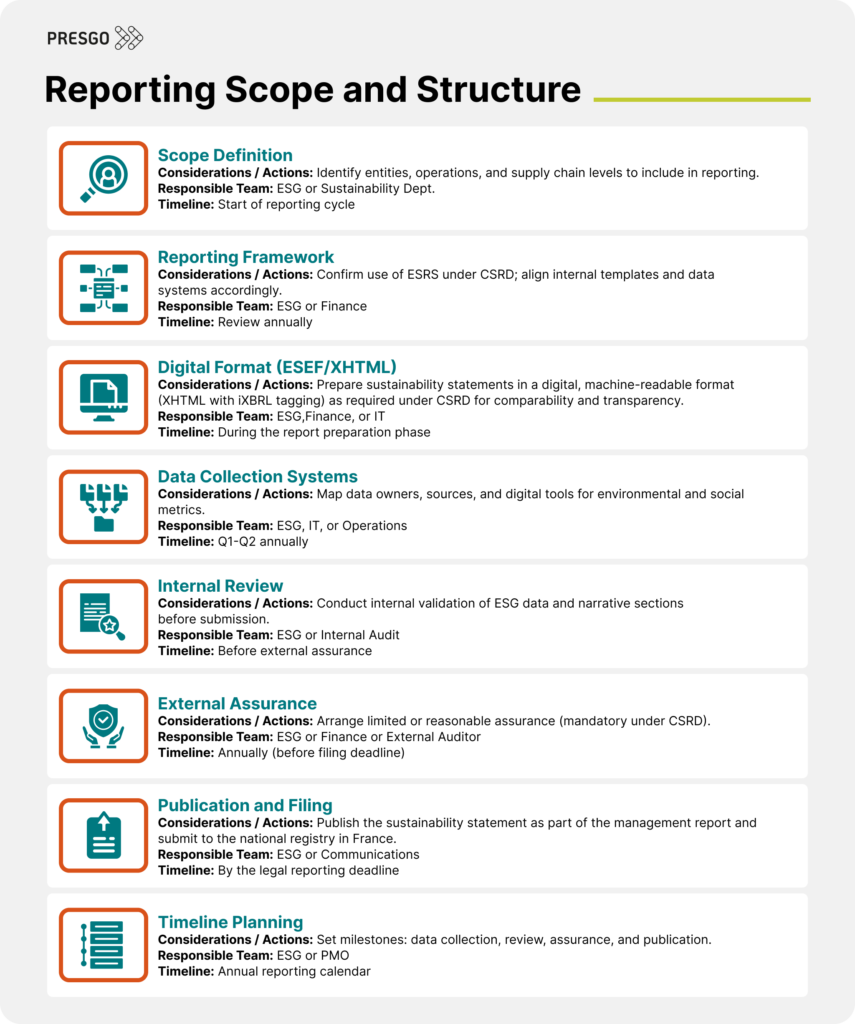

2. Reporting Scope and Structure

Next is to define the scope. Under the CSRD, companies must report using the ESRS. This establishes the structure and content of the disclosures. This is also the time to decide which business areas and supply chain levels are included in your ESG reporting. Keep your scope consistent over time so it is easier to compare progress. For the Renault Group, its Life Cycle Assessment (LCA) covers the full vehicle life cycle from raw material sourcing and the pre-design stage.

Here is the breakdown of reporting scopes and structures.

3. Data Mapping and Collection

Collect reliable data. Gather numbers and facts that reflect your operations. These are some examples of ESG metrics, including energy use, emissions, DEI, labour practices, and ethics. This is also when you look into concerns related to your data.

Who is responsible: ESG Data Manager, Finance, Human Resources (HR), and Health, Safety, and Environment (HSE)

This table outlines the key ESG metrics often tracked and where that information is typically sourced.

4. Stakeholder Engagement

Talk to your employees, clients, investors, and partners. Their feedback helps compose a report that feels relevant and credible from multiple perspectives.

Who is responsible: Communications, Investor Relations, HR

What to consider: Who are your main stakeholders? How do you gather and act on their feedback?

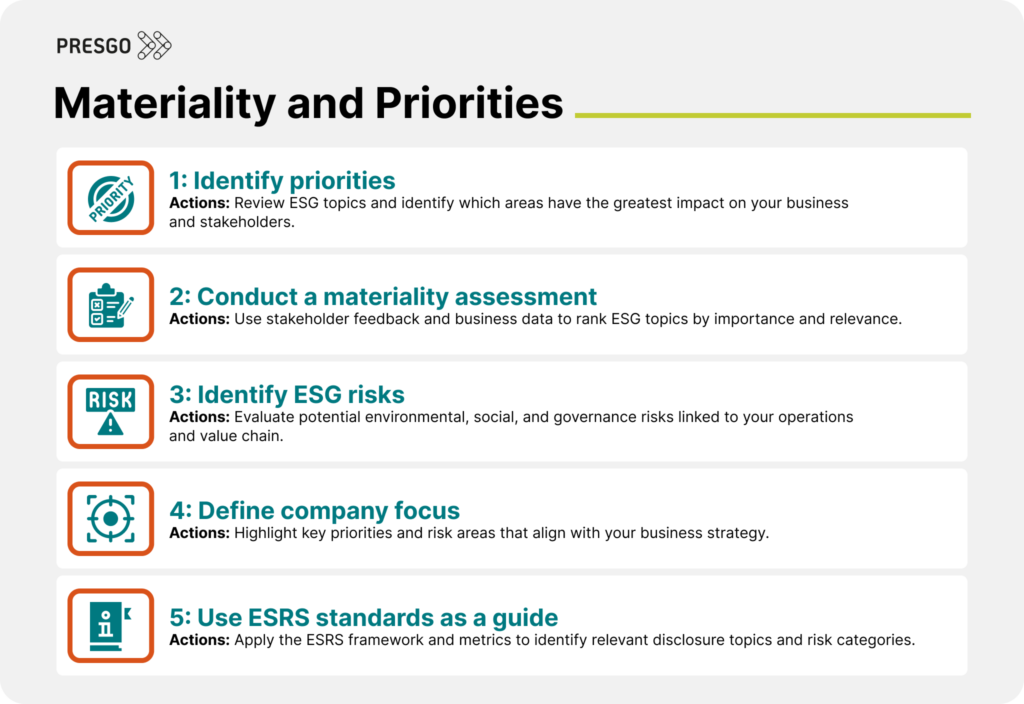

5. Materiality and Priorities

Identify ESG priorities, materiality, risks, and ESRS metrics. Not all ESG topics carry the same weight. Use a materiality assessment to focus on what matters most to your business and stakeholders.

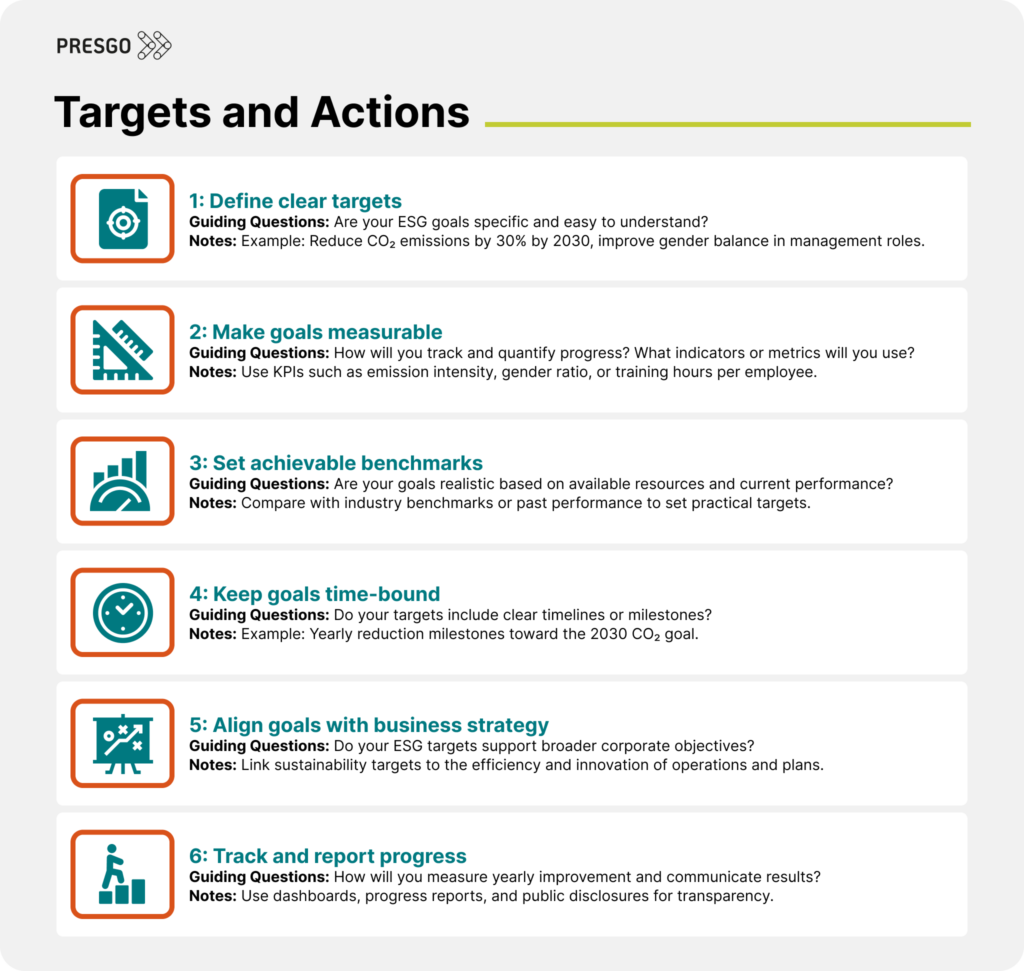

6. Targets and Actions

Set measurable goals. Turn insights into targets and workable actions, like improving gender balance in management and cutting GHG emissions by a set percentage. Such is the case for Air France’s priority, which sets its target of reducing CO₂ by 30% in 2030. It helps to make these targets achievable by tracking progress and being transparent about what’s still in progress.

7. Continuous Improvement

After publication, review and gather feedback. Note what worked or didn’t and what needs refining. ESG reporting is a continuous cycle. Following an ESG checklist creates institutional memory for the next reporting years.

Who is responsible: Sustainability Department, Internal Audit

What to consider: What feedback did you receive? How will you use it to strengthen next year’s report?

How to Use the ESG Checklist Template

Use the checklist as a practical guide throughout your reporting cycle, keeping tasks organised, responsibilities clear, and progress visible throughout the reporting cycle.

- Start with setup: Save a copy of the checklist and assign task owners before the reporting cycle begins.

- Work step-by-step: Treat each line as an action item, updating the status, adding notes, and linking supporting documents as you go.

- Track progress regularly: Review it in team check-ins to spot roadblocks, delays, or missing information early on.

- Use it for coordination: Share the file paths to data sources and review materials for easy follow-up. ESG software can streamline the process by keeping all data and evidence in one place.

- Update after submission: Record completion dates and lessons learnt once the report is filed and published.

- Reuse next year: Keep the checklist as your base for the next reporting cycle, adjusting tasks and timing as regulations also evolve.

When used consistently, the checklist becomes part of your reporting flow. It’s clear, repeatable, and audit-ready. Many teams also utilise ESG software and technology to streamline the process, centralising data, automating updates, and simplifying tracking.

FAQs on ESG Checklists

What are the ESG reporting requirements in France?

French companies must comply with the CSRD, which uses the ESRS as the main framework. Depending on their size and activity, some are also covered by the SFDR, EU Taxonomy, and CSDDD. Reports must include double materiality analysis, receive limited assurance, and be submitted digitally to the Autorité des marchés financiers (AMF).

How do you create an ESG checklist template?

Most companies design their own checklist instead of relying on public templates. It should map out the reporting process, covering regulations, data sources, timelines, and team responsibilities, to keep tasks clear and progress trackable throughout the ESG cycle.

What is ESG software, and how can it help in creating a checklist?

ESG software streamlines the reporting process by automating data collection, tracking reviews, and linking everything to your checklist. Platforms like Presgo centralise disclosures, documentation, and workflows, making reporting faster, more reliable, and easier to audit.

Fast-track Your ESG Report Checklist with Presgo

ESG reporting software often offers prebuilt ESG templates aligned with standards like ESRS, GRI, or TCFD recommendations and integrates with energy systems, HR systems, or procurement platforms. Many ESG reporting software tools provide built-in review workflows, audit trails, version tracking, and extract features for auditors.

Presgo is an ESG software designed around the logic of checklists and audit lifecycle support. Here’s how it can reduce friction in going through each step in ESG reporting.

- Prebuilt ESRS-Aligned Templates and Libraries: Presgo comes with standard ESRS disclosure modules aligned with other global frameworks. This means your checklist maps directly to configured templates, all in one place.

- Automated Data Ingestion and Integration: Instead of updating spreadsheets manually, Presgo can extract data from documents and management systems. That streamlines the data flow and minimises manual errors.

- Workflow and Reviewing: Presgo allows you to define who reviews what, in what order, and allows gate or review points. Changes and comments are tracked for clear audit trails.

- Comparison and Benchmarking: As your company’s ESG reporting matures, Presgo helps you compare cycles, test scenario analysis, and benchmark your performance relative to peers. This brings insights and strategies beyond compliance.

- Assurance support and auditor interface: The tool can package the data, change logs, and underlying metadata. This speeds the internal and external ESG audit and verification processes.

- Collaboration and stakeholder access: With comment threads, read-only dashboards for leadership or external stakeholders, and centralised feedback, multiple disconnected file versions and miscommunication can be avoided.

A solid checklist keeps your ESG reports on track. Presgo gets you through it faster and smarter. Request a product walk-through of Presgo today.