Contents

- What is a materiality assessment in sustainability?

- How is materiality assessment addressed under Philippine regulations?

- Why does materiality matter for Philippine companies now?

- Why start with materiality assessment before ESG reporting?

- How does materiality assessment fit into the risk management process?

- Why are the biggest ESG risks outside your company’s control?

- What does a well-run materiality assessment produce?

- Start Your Materiality Assessment for Effective ESG Strategy in the Philippines with Presgo

- Request a Free Materiality Topic Review

The Philippines regularly faces weather calamities, supply chain vulnerabilities, governance concerns, and labour-related issues. Because businesses operate within this environment, these national realities affect the stability, cost, and competitiveness of Philippine companies.

At the same time, global expectations toward environmental, social, and governance (ESG) disclosures have scaled up in the Philippines. The country’s voluntary sustainability disclosures have evolved into structured regulatory and investor observation of a company’s response to ESG challenges.

With the recent ESG disclosure mandates, companies may jump straight to compliance and template reporting without the substantial data and priority-focused strategy. For Philippine companies facing that uncertainty and wondering where to begin, studying materiality offers clarity before taking care of the rest. This is where materiality assessments play a crucial role.

What is a materiality assessment in sustainability?

Materiality assessment, in a sustainability context, is a structured process that identifies which ESG topics are most significant and relevant, taking into account the risks and opportunities and possible implications. For a company starting sustainability materiality assessment in the Philippines, the question is this: Which ESG issues actually matter to the company and stakeholders?

This assessment involves producing a clear list of material topics to address, defined boundaries showing where impacts occur, and documented reasoning for why certain issues were selected. The data creates a materiality matrix that maps the identified ESG issues, based on their stakeholder importance and business impact. This visualization then shows which topics require the greatest focus. By doing this, the company also determines what to disclose, leading to a clearer ESG reporting process.

Types of Materiality

Materiality assessment can have different focuses, which also depend on the ESG framework applied. These focuses can vary from:

| Materiality Type | Description | Framework Application |

| Impact Materiality | Addresses how company operations and initiatives impact the economy, society, and the environment | Global Reporting Initiative (GRI) |

| Financial Materiality | Focuses on sustainability-related risks and opportunities that could reasonably affect a company’s enterprise value | ISSB’s IFRS S1 and S2 |

| Double Materiality | Combines both impact and financial perspectives, considering both the impact on society and how sustainability issues affect the company. | Corporate Sustainability Reporting Directive (CSRD); European Sustainability Reporting Standards (ESRS) |

How is materiality assessment addressed under Philippine regulations?

The Securities and Exchange Commission (SEC) in the Philippines has developed and introduced guidelines that tackle financial materiality. In 2019, the SEC published sustainability reporting guidelines for Philippine companies, where ESG disclosures and materiality were handled in a comply-or-explain arrangement. This didn’t push for strong consistency, scope, and sustainable impact that could cover the larger economic landscape of the country.

It later introduced the Philippine Financial Reporting Standards (PFRS) in December 2025, through the Memorandum Circular 16, Series of 2025.

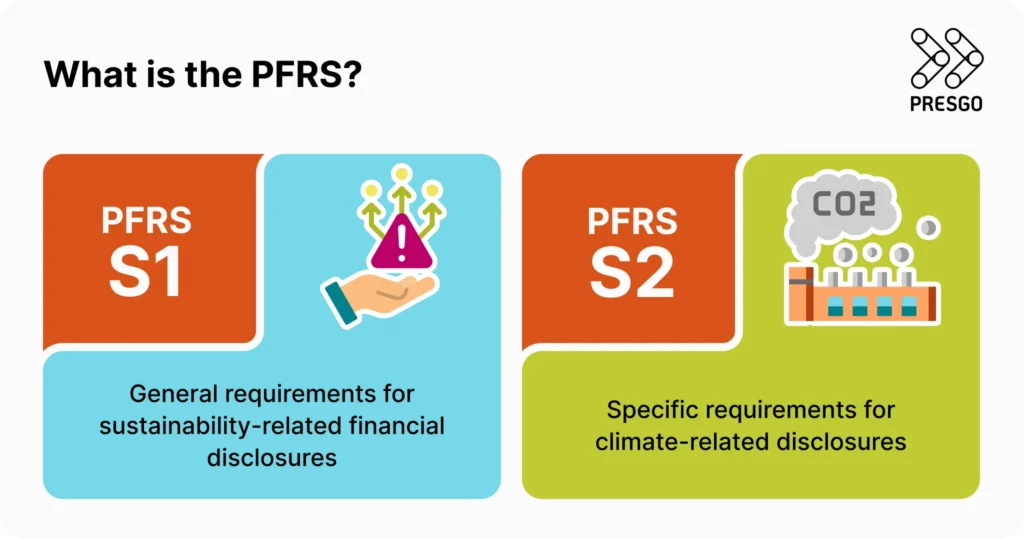

What is the PFRS?

PFRS is the Philippine-specific sustainability reporting framework adopted from the International Financial Reporting Standards (IFRS) Foundation’s sustainability disclosure standards, IFRS S1 and S2. The adoption is intended to globally align Philippine companies’ sustainability reports and improve the integration of sustainability-related risk and opportunities into financial reporting. The PFRS identifies two complementary disclosure standards:

PFRS S1

The S1 standard establishes the foundation for all sustainability reporting. It requires companies to report sustainability risks and opportunities that affect the cash flows, access to finance, or cost of capital. This standard covers governance structures, strategy, risk management processes, and performance metrics across all material sustainability topics.

PFRS S2

The S2 standard particularly zooms in on climate-related risks and opportunities. It mandates disclosure of greenhouse gas (GHG) emissions across scopes 1, 2, and 3. It also includes climate-related physical and transition risks, resilience under different climate scenarios, and targets for emissions mitigation. Think of S2 as the detailed chapter on climate within the broader S1 framework.

Get Free Assessment Today

Why does materiality matter for Philippine companies now?

Local context influences which issues become material for Philippine companies.

In the 2024 World Economic Forum report, 66% of respondents list “extreme weather events” as the top global risk, even in the next 10 years. In 2025, the Philippines was placed first for flood risk, given how it is positioned in one of the world’s most climate-vulnerable regions. This situation affects Philippine companies on a larger scale as typhoons and rising temperatures disrupt supply chains, damage facilities and resources, and strain energy systems. Additionally, procurement practices, anti-corruption measures, labor standards, and community impacts also shape corporate resilience.

In the Philippine Financial Reporting Standards, the SEC is now more critical of companies articulating how climate and environmental impacts translate into financial risk. These are what the PFRS highlights:

- A stronger alignment with globally recognized standards, particularly the IFRS S1 and S2.

- Refined and clearer disclosure requirements on climate and scopes 1 and 2 emissions.

- A tiered and gradual implementation roadmap across a wider scope, extending beyond publicly listed companies (PLCs).

The implementation requires PLCs in the Philippine Stock Exchange (PSE) and the Philippine Dealing & Exchange Corporation (PDEx) and large non-listed entities (LNLs) to adopt PFRS S1 and S2 in different timelines:

| Category | Scope of market capitalization (as of December 2025) | Timeline for disclosure standards adoption |

| Tier 1 | – PLCs listed in the PSE exceeding PHP 50 billion | 2026: First adoption 2028: Full adoption (including scopes 1 and 2 emissions reporting) |

| Tier 2 | – PLCs listed in the PSE under PHP 50 billion but more than PHP 3 billion | 2027: First adoption 2029: Full adoption (including scopes 1 and 2 emissions reporting) |

| Tier 3 | – PLCs listed in the PSE with PHP 3 billion or under – PLCs listed in the PDEx – LNLs with more than PHP 15 billion in revenue | 2028: First adoption 2030: Full adoption (including scopes 1 and 2 emissions reporting) |

Why start with materiality assessment before ESG reporting?

When companies jump straight into reporting frameworks and tools, it often creates misalignment and wastes resources. Here’s what materiality gives you first:

Avoids irrelevant data connection

Materiality assessment stops companies from burning resources on irrelevant data. Take a manufacturing company collecting water use data across all facilities. A materiality assessment reveals that only three locations face real water stress. Now data collection can zero in on actual risk, saving time and effort.

Boosts team and executive alignment

Materiality shows teams why they are collecting specific data and how their work connects to the risk management strategy and ESG reporting. This creates shared responsibility among teams and informed decision-making under leadership, making prioritization easier across departments.

Prevents unnecessary rework

ESG regulations keep changing. The move from the 2019 SEC sustainability reporting guidelines to the latest 2025 version shows how frameworks mature. Companies that know their material issues adapt to new standards, IFRS S1 and S2 and CSRD, without scrambling to rebuild data systems or reporting formats.

Leverage transition reliefs effectively

The SEC’s tiered approach gives companies breathing room through transition periods. Those who’ve already done materiality assessments can meet requirements and deadlines for the long haul, breaking the workload into manageable pieces.

How does materiality assessment fit into the risk management process?

A materiality assessment is often the earliest point at which a company can spot significant ESG risks before they affect costs, operations, or revenue. Where traditional risk assessment examples focus on operational disruptions, market volatility, or regulatory compliance, a materiality assessment widens that lens. It reveals ESG risks that carry the same financial and operational weight, from climate exposure to supply chain liabilities.

The climate-related flooding and disruptions represent an ESG risk that falls within the same enterprise risk category as traditional operational disruptions. Through a materiality assessment, such climate exposure can be identified early as significant sustainability-related risks that may affect assets, revenue, and long-term resilience.

This was evident in typhoon Kristine in 2024, which caused nearly PHP 79 million in agricultural damages in irrigation systems, machinery, and other infrastructure. By recognising climate vulnerability as a key priority, companies can proactively integrate these risks into their broader risk management and mitigation strategies.

Identifying material issues early provides companies with a clearer view of what requires support, extensive improvement, and added security. It lets companies prioritize the needs of the company and its supply chain and advance its overall risk management.

Why are the biggest ESG risks outside your company’s control?

For most companies, the biggest ESG risks live in the value chain. Scope 3 emissions, the indirect impacts from sourcing materials, working with suppliers in disaster-prone areas, and everything else that happens outside facilities, make up the bulk of risk exposure. Companies don’t control these risks directly, but they affect operations and sustainability goals at scale.

In the Philippines, industries built on agriculture, construction, and manufacturing face serious scope 3 challenges. The country’s exposure to natural disasters and climate risks creates ripple effects across entire value chains, affecting product quality, driving up costs, and bringing environmental and regulatory consequences.

Scope 3 emissions dominate because they reach far beyond direct company operations. Supplier violations, material scarcity, transportation emissions, and downstream impacts — all these can destabilize your business when supply chains break down during disasters. Companies that have a complex supply chain and ignore these indirect risks are also putting their operations at risk.

Incorporating Scope 3 Risks into Materiality Assessments

Building these external risks into materiality assessments moves ESG beyond compliance and into real risk management. As government and regulators demand better insurance coverage and disaster response, businesses need to face the indirect risks lurking in their supply chain’s capacity. When you identify these risks early, you can cut potential losses, build disaster resilience into continuity plans, and adapt your strategy as conditions shift.

The private sector is stepping up on climate adaptation and resilience with its materiality assessment. Nickel Asia Corporation (NAC), one of the Philippines’ largest lateritic nickel ore producers, treats scope 3 emissions as a business and ESG issue. With supplier engagement, the company identified ESG issues for its GRI-aligned sustainability reporting. In this way, NAC is showing the kind of ESG prioritization it builds into its materiality assessment process. This positions NAC’s materiality assessment as an active part of how the company identifies and manages operational and supply chain risk. It is a direct integration of ESG materiality into its enterprise risk management process.

Get Free Assessment Today

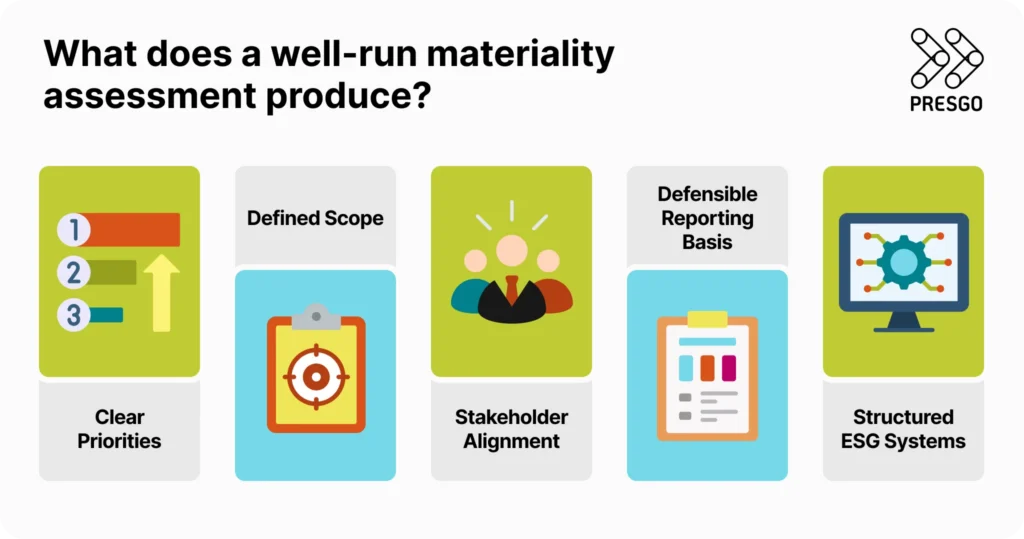

What does a well-run materiality assessment produce?

A well-executed ESG materiality assessment delivers key outputs that shape every future ESG decision. It drives focus, ensures alignment, and sets a strong foundation for technology adoption.

- Clear Priorities: The assessment identifies the key topics that matter most to your business, guiding resource allocation and strategy.

- Defined Scope: It clarifies which operations, geographies, and supply chain segments are most affected by ESG risks, eliminating wasteful, one-size-fits-all approaches.

- Stakeholder Alignment: Engaging stakeholders in defining material issues ensures everyone is on the same page, minimizing future resistance to initiatives.

- Defensible Reporting Basis: Materiality provides solid evidence for reporting decisions, showing priorities are based on analysis, not arbitrary choice.

- Structured ESG Systems: With clear priorities, companies can build effective data collection, metrics, targets, and governance around material topics, enhancing ESG technology adoption.

Start Your Materiality Assessment for Effective ESG Strategy in the Philippines with Presgo

For Philippine companies tackling ESG, a materiality assessment is the smartest and safest starting point. Setting priorities makes data collection and reporting intentional. This creates more focused and impactful sustainability efforts that go beyond compliance in the local context.

ESG software and technology simplify and guide companies through materiality assessments and throughout the reporting process.

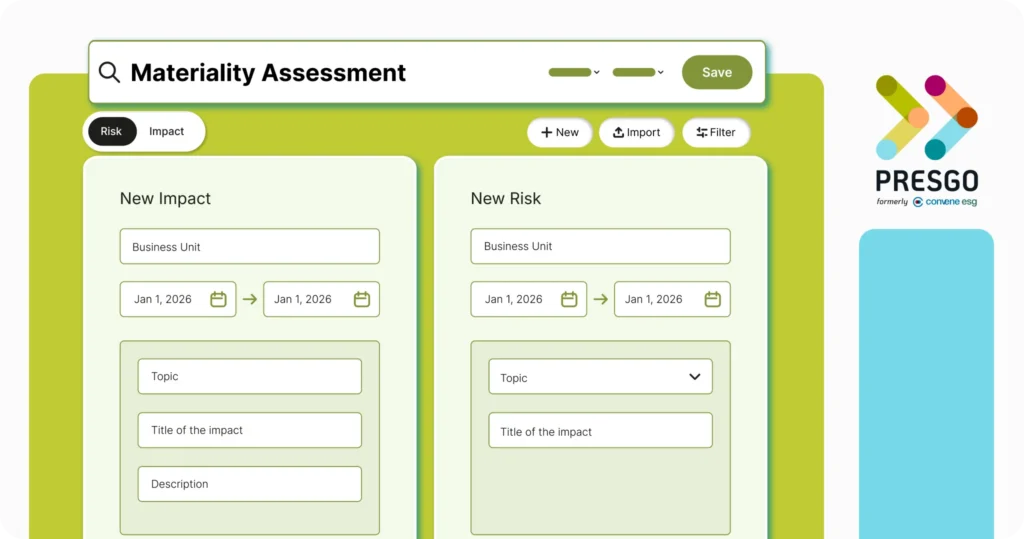

Presgo is an AI-first ESG reporting software built to guide companies through this materiality-driven approach. The platform refines ESG reporting workflows, centralizes data, automates processes, and aligns with global standards.

With Presgo’s ESG tools and materiality solutions, you gain:

- AI-supported materiality assessment: Identify what matters most with a structured materiality process. Presgo’s AI-powered analysis generates heatmaps that highlight ESG issues with the highest impact.

- Carbon calculator: Measure scopes 1, 2, and 3 emissions accurately using verified factors, such as from the GHG Protocol, IPCC, US EPA, UK DEFRA, and IGES. Presgo refines scope 3 reporting through configurable surveys, AI scoring, and automated summaries.

- Supplier ESG engagement: Collect and assess supplier ESG data through custom surveys and AI-assisted scoring narratives to get deeper insight into supplier performance and elevate scope 3 supply chain compliance.

- Disclosure hub with AI: Align disclosures with CSRD, GRI, IFRS S1 and S2, market-specific requirements, and local frameworks, such as the Philippines’ SEC sustainability reporting.

- Real-time progress and performance tracking: Monitor KPIs and ESG targets through interactive dashboards that reveal trends, gaps, and improvement opportunities. Track sustainability performance in real time and adjust strategies proactively to stay aligned with your commitments.

By using tools like Presgo, companies can make smarter, data-driven decisions and improve sustainability performance on what matters.

Request a demo today and start transforming your sustainability strategy with a clear focus on materiality.

Request a Free Materiality Topic Review

Get an assessment from a local ESG expert

"*" indicates required fields