Contents

- How often should materiality assessments be conducted?

- What are the common triggers that signal it’s time to review materiality?

- Best Practices to Ensure Validity of Materiality Assessments Across Reporting Periods

- How Sustainability Reporting Updates in the Philippines Influence Materiality Reassessments

- How Materiality Aligns with the ESG Reporting Cycle

- Conducting Your Materiality Assessment Cycle with Presgo

Materiality assessments in ESG reporting are often treated as a compliance milestone, an item in a checklist. But for Philippine companies guided by regulatory, investor, and stakeholder demands, materiality is more of a review cycle than a one-time deliverable.

Risks evolve, supply chains shift, and stakeholder expectations heighten. What was immaterial three years ago may now carry financial or regulatory impact. Revisiting a materiality assessment should go beyond redoing past work and help companies align their priorities with current realities.

Explore in this article the best time to conduct materiality assessments and how Philippine companies should reassess materiality to ensure alignment with sustainability efforts.

How often should materiality assessments be conducted?

Frameworks such as the International Sustainability Standards Board (ISSB) don’t specify a frequency, but how often to conduct a materiality assessment depends on changes in circumstances or information.

- Every 2-3 years: Conduct a full materiality assessment to comprehensively validate and recalibrate material topics.

- Annually: Carry out targeted updates to ensure material topics remain aligned with current impacts, risks, opportunities, and stakeholder expectations, especially for annual ESG reports.

- Special cases:

- Internal: Includes major changes in business operations such as mergers, acquisitions, and joint ventures, as well as leadership or board turnover.

- External: Includes regulatory changes, transitions to new reporting frameworks, or urgent industry-wide crises such as sector scandals, geopolitical conflict, severe inflation, or natural disasters.

- After each reassessment, sustainability teams should compare findings with previous results, identify recurring or emerging issues, track shifts in stakeholder priorities, and monitor evolving risks and opportunities.

Related Reading: Why Start with Materiality Assessments in ESG

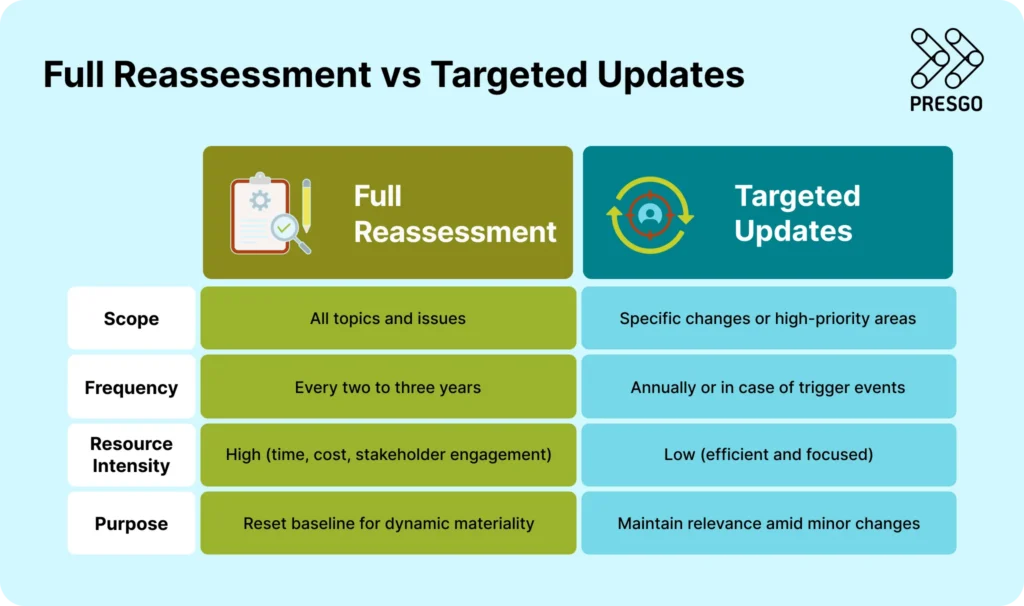

Full Reassessment vs Targeted Updates

A full ESG materiality analysis or reassessment typically involves a comprehensive reevaluation of all potential ESG risks, or stakeholder issues. These are performed to capture major shifts in business context, regulations, or priorities.

Meanwhile, targeted updates focus only on specific changes such as new risks, stakeholder feedback, or recent events. These are done without needing to revisit the entire assessment, and allow for quicker annual or ongoing adjustments.

These approaches to materiality assessments ensure topics and issues remain relevant to the organization and its stakeholders while preventing redundancy. Unnecessarily conducting frequent reassessments may lead to inefficient use of resources and confusion with priorities.

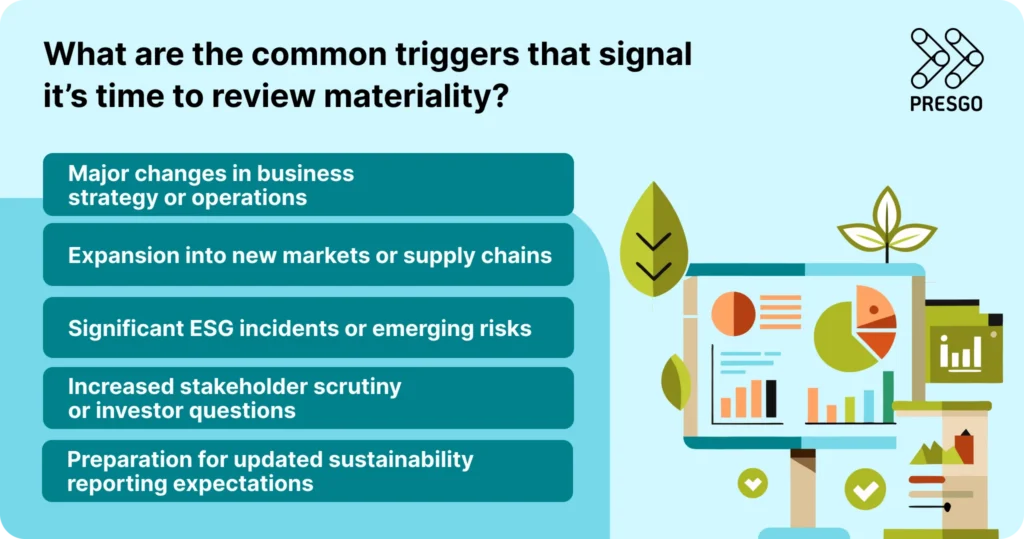

What are the common triggers that signal it’s time to review materiality?

Materiality reassessments may be due if a specific event or shift in circumstances impacts issues relevant to an organization’s sustainability strategy. These “triggers” may result in potential changes to stakeholder expectations, regulatory landscapes, or operations, subsequently requiring a reassessment of priorities for the organization. Some common triggers are:

- Major changes in business strategy or operations, such as mergers or the adoption of new technologies.

- Expansion into new markets or supply chains, such as entry to new geographies. Philippine exporters, for example, must adapt to the EU’s Carbon Border Adjustment Mechanism (CBAM), which focuses on supply chain emissions.

- Significant ESG incidents or emerging risks, such as hazardous chemical spills or regulatory violations, including data breaches, as well as climate events.

- Increased stakeholder scrutiny or investor questions, such as demands from investors, NGOs, or communities, may require materiality updates. In the Philippines, 79% of Asia-Pacific investors consider ESG a major factor in their decisions.

- Preparation for updated sustainability reporting expectations, such as the newly adopted IFRS-based Philippine Financial Reporting Standards (PFRS) on Sustainability Disclosures, in early 2026. The PFRS on Sustainability Disclosures requires companies to report sustainability-related financial disclosures (PFRS S1) and climate-related risks and opportunities (PFRS S2) based on the ISSB standards.

For example, Philippine conglomerate Ayala Corporation continuously refreshes its materiality sustainability topics. In 2023, the company adopted the double materiality approach, with results published in 2024 to help reaffirm the company’s sustainability strategy and activities.

Meanwhile, Nickel Asia Corporation (NAC) refreshes its materiality assessment validity through a comprehensive assessment every three years. This aligns with global best practices such as the GRI and the SASB frameworks. The material topics are then reported in NAC’s annual sustainability reports to ensure transparency.

Best Practices to Ensure Validity of Materiality Assessments Across Reporting Periods

While full reassessments aren’t required annually, teams should still review existing assessments to ensure they align with stakeholder priorities and expectations and business risks and impacts. Some best practices teams should adopt to ensure the continuous validity of outputs include:

- Annual review and continuous monitoring: Teams should reconfirm material topics in the event of any priority shifts. If significant changes (mergers and acquisitions, entry into new markets, or shifts in key suppliers) occur, a full, in-depth reassessment may be necessary.

- Establish a repeatable methodology: Teams should document the methodology used for identifying and evaluating topics to standardise the process and ensure easier replication in future assessments. Modern ESG tools offer automated and data-driven features to help analyze trends and stakeholder feedback, improving accuracy and efficiency in the long term.

- Maintain dynamic stakeholder engagement: Foster consistent and ongoing engagement with stakeholders to identify emerging issues and concerns as they arise. It’s also important to update the list of stakeholders to ensure all relevant groups are involved in the process.

- Integrate with risk management and strategy: Findings from the materiality assessment should be aligned with the corporate risk management framework to ensure data remains relevant alongside global, long-term trends. This includes technological shifts or geopolitical changes that could change the materiality of specific issues.

- Document changes in materiality: In case of changes in material topics, these changes must be disclosed and properly documented to ensure auditability for regulators and investors.

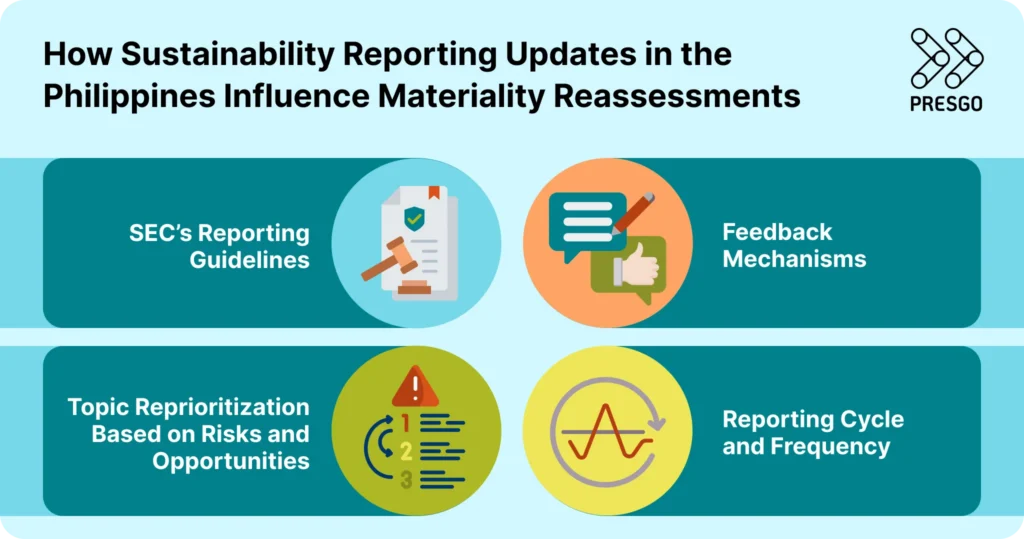

How Sustainability Reporting Updates in the Philippines Influence Materiality Reassessments

For sustainability reporting in the Philippines, changes and updates under SEC regulations influence materiality reviews by providing stakeholder feedback, performance data, and regulatory alignment needs, feeding into the assessment cycle.

SEC’s Reporting Guidelines

The SEC’s Memorandum Circular No. 4 required publicly listed companies (PLCs) to conduct materiality assessments on a comply-or-explain basis. Memorandum Circular No. 16, introduced in 2025, restructured the process based on ISSB disclosure requirements. This makes sustainability reporting mandatory for PLCs and Large Non-Listed Entities (LNLs) under the PFRS S1 and S2. Reports filed with SEC Form 17-A (SuRe Form) must detail this process to ensure that disclosures align with ISSB IFRS S1/S2 standards starting 2026.

Feedback Mechanisms

Stakeholder input from sustainability reports can reveal changes in concerns and priorities. To adjust, companies will need to reassess material topics annually or based on triggers such as regulatory changes. This ensures disclosures remain aligned with current risks, public expectations, and regulatory requirements instead of relying on outdated assessments.

Topic Reprioritization Based on Risks and Opportunities

Material topics should be reprioritized when a company’s risk exposure, strategy, or regulatory environment changes. In the Philippines, evolving requirements from the SEC and alignment with IFRS S1 and S2 may impact climate, governance, and financially material sustainability risks. Frequent climate events, such as typhoons, can also shift risk and opportunity profiles. Periodic reassessment ensures disclosures remain accurate.

Reporting Cycle and Frequency

Reporting closes the loop by validating material topics against outcomes, with the SEC expecting periodic reviews (at least annually for compliance) to incorporate feedback aligned with global frameworks. By standardising an annual review process according to the required reporting calendar, companies can prevent outdated disclosures and potential regulatory or investor scrutiny.

How Materiality Aligns with the ESG Reporting Cycle

Materiality helps prioritize disclosures that impact stakeholders and business prospects and can improve the efficiency and consistency of ESG teams throughout the reporting cycle.

Using Materiality as an ESG Anchor

Materiality helps anchor ESG reporting by identifying topics with significant economic, environmental, or social impacts on the company and its stakeholders. Listed companies must detail their materiality process in SEC reporting templates to rank issues by importance. This ensures that disclosures focus on the most important matters, such as those affecting prospects according to IFRS S1 standards.

Boosting Reporting Efficiency

Conducting materiality reviews well ahead of the annual ESG reporting cycle also streamlines preparation by locking in priorities early. Regular, proactive assessments prevent last-minute data scrambles and align with dynamic updates recommended in best practices, mirroring processes used by companies like multinational conglomerate San Miguel Corporation. This timing reduces resource strain during peak reporting periods mandated by the Philippine Stock Exchange (PSE).

Preventing Reactive Deadline Changes

A robust materiality assessment upfront prevents companies from simply being reactive to tight timelines, such as the SEC Philippines sustainability report deadlines. Establishing fixed material topics also helps filter out non-essential topics. For listed companies in the country, this discipline ensures compliance without compromising report quality, as emphasised in the PSE circulars.

Supporting ESG Consistency

Materiality fosters consistent narratives across sustainability reporting years by maintaining stable material topics unless significant operational changes occur, as seen in assessments by Nickel Asia and San Miguel where priorities held steady. Annual reaffirmations document continuity, building stakeholder trust through transparent evolution rather than volatility. This approach aligns with SEC expectations for ongoing relevance in sustainability disclosures.

Conducting Your Materiality Assessment Cycle with Presgo

In an ever-evolving landscape, revisiting a materiality assessment should not be triggered by panic, headlines, or sudden regulatory pressure. Instead, materiality assessments should be a matter of governance discipline.

Presgo is an AI-first ESG reporting tool designed to help companies centralize ESG data, conduct materiality assessments, and ensure organizations remain aligned with global and local reporting frameworks. Key Presgo modules include:

- Materiality Assessment: Establish a repeatable methodology for your ESG team by enabling them to gather stakeholder input, score impacts, and prioritize ESG topics through documented workflows. The Materiality Assessment module directly supports SEC expectations for materiality-based disclosures and SuRe Form reporting.

- Data Hub: Centralize ESG data across teams and departments, and maintain validation trails. Over time, the Data Hub allows companies to reassess whether previously identified topics remain material based on updated performance data, risks, or operational changes.

- Disclosure Hub: As SEC reporting evolves toward structured templates and PFRS, reassessment outcomes must translate consistently into reporting narratives. The Disclosure Hub module helps map disclosures to regulatory requirements.

- Report Builder: Revisiting a materiality assessment is more than simply reprioritizing ESG topics. Presgo’s Report Builder connects validated ESG data, material topics, and disclosure narratives into a comprehensive reporting workflow. Philippine companies reporting across overlapping frameworks such as the SEC SuRe Form and ISSB-aligned disclosures can export reports in regulator-ready formats such as PDF or XBRL tagging.

Book a demo today to learn how Presgo can support your organization’s materiality review!