Contents

- What is materiality assessment in the Philippine context?

- How does materiality assessment make reporting easier for Philippine companies?

- What Makes an Effective Materiality Assessment: Best Practices from Philippine Companies

- How do leading Philippine companies approach scope 3 topics in their materiality assessments?

- Build a Successful ESG Materiality Assessment with Presgo

The recent developments in mandated sustainability disclosures in the Philippines are increasing scrutiny of companies to a greater extent. Companies can compile extensive topic lists, color-code their materiality matrix, and cover as many material topics as possible. But these don’t always translate into a strong materiality process for the actual reporting.

The notable sustainability disclosures in the Philippines stand out for clearly focusing on business and sustainability issues. They mirror the same prioritisation seen across Asia-Pacific boardrooms, where the EY board priorities report of 2025 identifies sustainability integration among five core board focus areas. Climate-related disruptions, resource scarcity, and ecosystem risks remain among the greatest threats facing the region over the next decade. As these pressures grow and evolve, companies are expected to integrate these risks and issues into their core business strategy. The strongest materiality assessments in sustainability reporting apply that same logic.

What is materiality assessment in the Philippine context?

A materiality assessment is the company’s way of prioritising environmental, social, and governance (ESG) topics that shape business decisions and performance. It is a structured process that tests which sustainability topics carry real weight, based on evidence of risk and opportunity, and where impacts occur in the value chain. The output is usually a short, supported set of material topics, visualized in a materiality matrix.

In the Philippines, materiality has evolved into a concern for disclosure and governance. The country’s Securities and Exchange Commission (SEC) introduced sustainability reporting guidelines in 2019 to formalize ESG reporting among publicly listed companies. In December 2025, SEC issued Memorandum Circular No. 16, Series of 2025, adopting the Philippine Financial Reporting Standards (PFRS) on Sustainability Disclosure. These standards, aligned with those of the International Sustainability Standards Board, replace the earlier guidelines, expand coverage to large non-listed entities, and introduce phased mandatory adoption beginning in fiscal year 2026. The framework also sets a timeline for limited assurance on Scope 1 and Scope 2 greenhouse gas emissions two years after adoption for each reporting tier.

The introduction of PFRS S1 and S2 represents a broader shift in how materiality assessments are approached in the Philippines. Rather than treating ESG reporting primarily as a stakeholder-focused narrative, the new framework emphasizes sustainability information that is material to investors and capital markets. Companies are now expected to identify and disclose sustainability-related risks and opportunities that could affect enterprise value and to integrate these considerations into governance, strategy, and risk management processes while strengthening the data systems and internal controls that support disclosures.

For companies that previously conducted materiality assessments under the SEC’s 2019 sustainability reporting guidelines, this shift does not invalidate existing work but changes how materiality must be interpreted and disclosed. Many Philippine companies previously followed impact-based approaches such as the Global Reporting Initiative materiality process, which prioritized ESG topics through stakeholder surveys and impact scoring. These assessments can still serve as a foundation, but companies must now reassess them through a financial lens by identifying sustainability-related risks and opportunities that could affect enterprise value, cash flows, cost of capital, or access to finance. In practice, many organizations are conducting “materiality refresh” exercises—mapping existing ESG topics to financial risks and opportunities and integrating them into enterprise risk management rather than restarting the process from scratch.

How does materiality assessment make reporting easier for Philippine companies?

Companies investing in an effective materiality assessment find that the rest of the sustainability and reporting process becomes easier. Here is how a strong materiality assessment translates into reporting advantages:

- Clear scope reduces data overload: When a company knows its top material topics, it knows what data to collect, from whom and where, and at what frequency. This minimizes unnecessary and inconsistent data that makes reporting harder in the long run.

- ESG systems support execution, not discovery: Companies that define material topics first can build data collection and governance structures around those priorities. With PFRS S1/S2 now adopted and mandatory from FY 2026 on a tiered basis, companies that already grounded their systems in materiality will adapt faster to the new placement, governance, and assurance expectations. Skipping this step can mean that a change in regulation or framework would disturb a company’s reporting process and require repeated restructuring.

- Structured data management and technology adoption: When there is an established foundation of material topics, it is easier to adopt ESG tools for automation, flagging anomalies, and supporting audit-ready reporting. In the case of Nickel Asia Corporation, it shifted from manual spreadsheet tracking to advanced ESG reporting software because of data inconsistencies and limited scalability.

- Reporting becomes repeatable and defensible: A well-documented materiality process gives your team something to refer to when auditors, investors, or regulators ask why certain topics were included or excluded. Under the SEC’s PFRS roadmap, some companies are to start adoption in 2026. A solid materiality assessment will give companies the foundation of their ESG topics to constantly and progressively base their reporting on.

What Makes an Effective Materiality Assessment: Best Practices from Philippine Companies

With the Philippine Financial Reporting Standards (PFRS) setting the baseline for materiality in the country, the emphasis goes from what affects stakeholders to what affects the business. The Philippine companies that run materiality assessments well share these practices.

1. Clear purpose and prioritisation from the start

The most effective materiality assessments identify the ESG topics that carry the most weight for the business, covering capital allocation, strategic planning, risk oversight, or target-setting. From these, the board and leadership decide where resources go, what needs a strategic response, and what gets reported in depth. This doesn’t necessarily mean other issues don’t exist. But those that do are backed by a supported and defensible case for their key material topics specific to the company’s context.

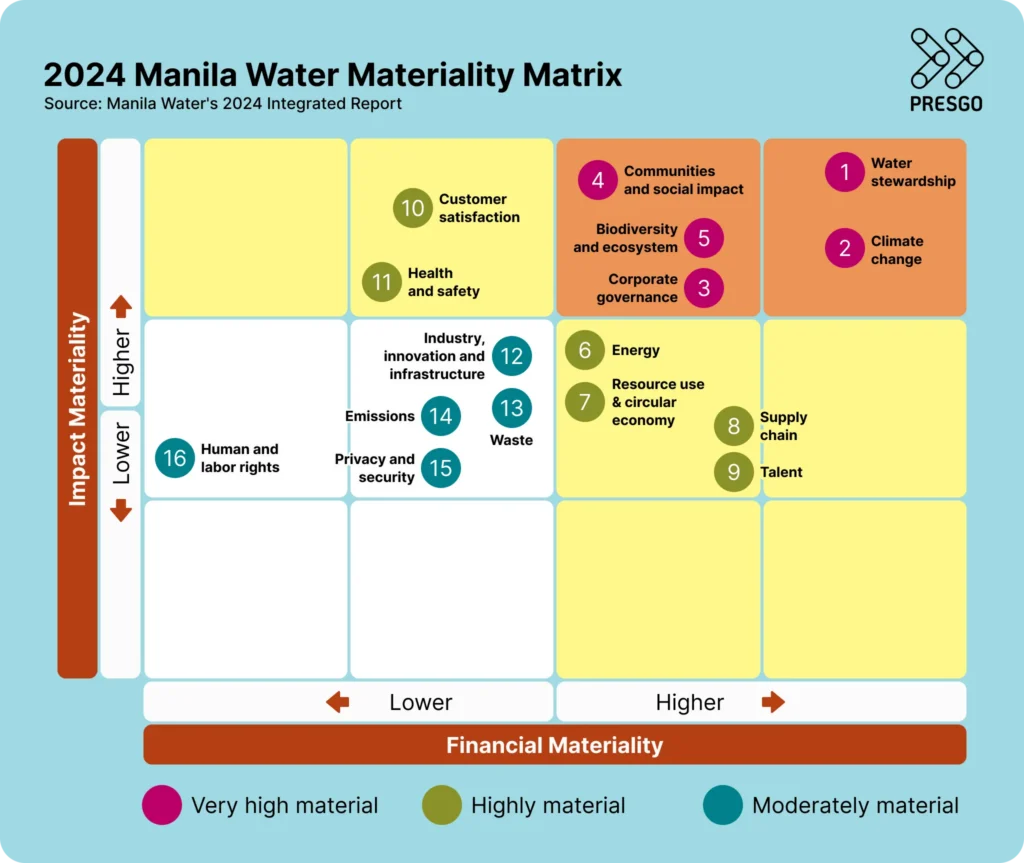

An example is the Ayala Corporation sustainability report’s materiality assessment, which followed a structured process before arriving at its final material topics. The Philippine holding company with investments in real estate, banking, telecommunications, energy, and infrastructure disclosed that it opened with an external landscape review. It scanned for major trends and growing risks, then measured its ESG priorities against comparable companies and global frameworks. Results were validated by several board-level committees, finalizing its material topics under the ESG pillars. The Manila Water, a water and wastewater company serving the Philippines and international markets, screened over 300 material issues before landing on 16 material topics. This prioritization shows a disciplined analysis and a focused approach on categories like corporate governance, business ethics, and climate risk. Its materiality matrix plots all these across financial and impact materiality axes, with water stewardship, climate change, and biodiversity clustering at the highest levels of significance across both dimensions.

Source: Manila Water 2024 Integrated Report

2. Logical classification of ESG issues

Leading companies group related issues under thematic pillars, instead of listing individual topics in isolation. These thematic pillars are typically drawn by the company leaders or sustainability team from their business context and established frameworks, such as the UN Sustainable Development Goals (SDGs), GRI standards, or industry-specific guidelines, as reference points. This makes the materiality rationale easier to follow and helps readers understand how topics connect in the business strategy.

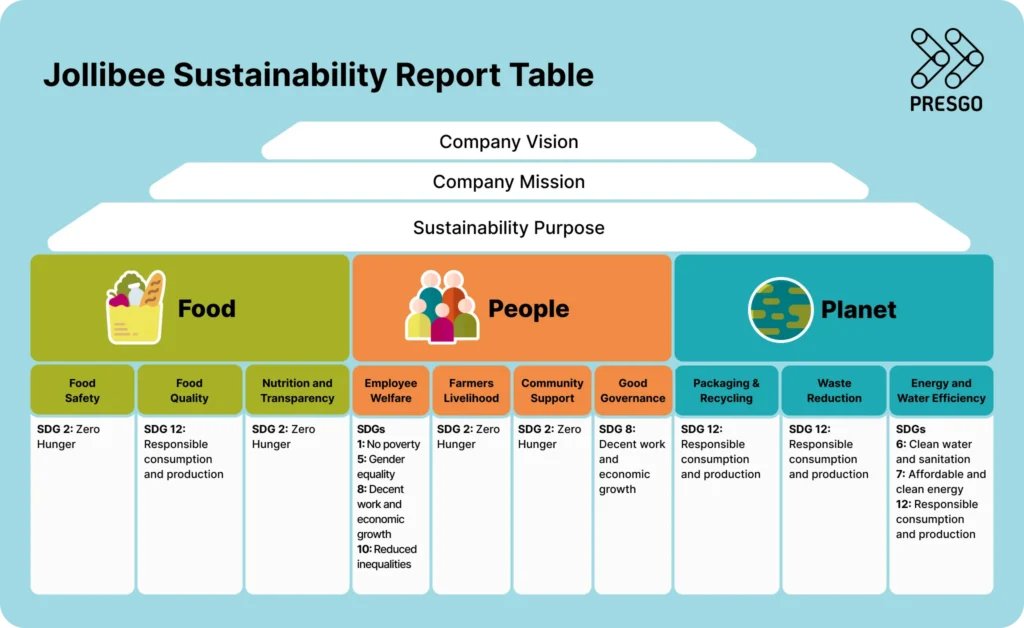

Jollibee Food Corporation is a Philippine-based global fast food chain that focuses its material issues on the main company pillars: food, people, and planet. These align with the UN SDGs and directly present the company’s operational footprint and where its materiality, performance, and overall sustainability disclosure content consistently revolve. Shown here is the summarized Joy of Tomorrow chart, from the Jollibee sustainability report, with specific material topics and their corresponding SDGs.

Source: Jollibee Food Corporation 2024 Sustainability Report

Investors, employees, suppliers, and regulators weigh each material topic differently. Effective materiality engagement surfaces those differences and documents them through stakeholder engagement. Collaboration, ownership, and an understanding of each material’s importance create more informed decisions and strategy.

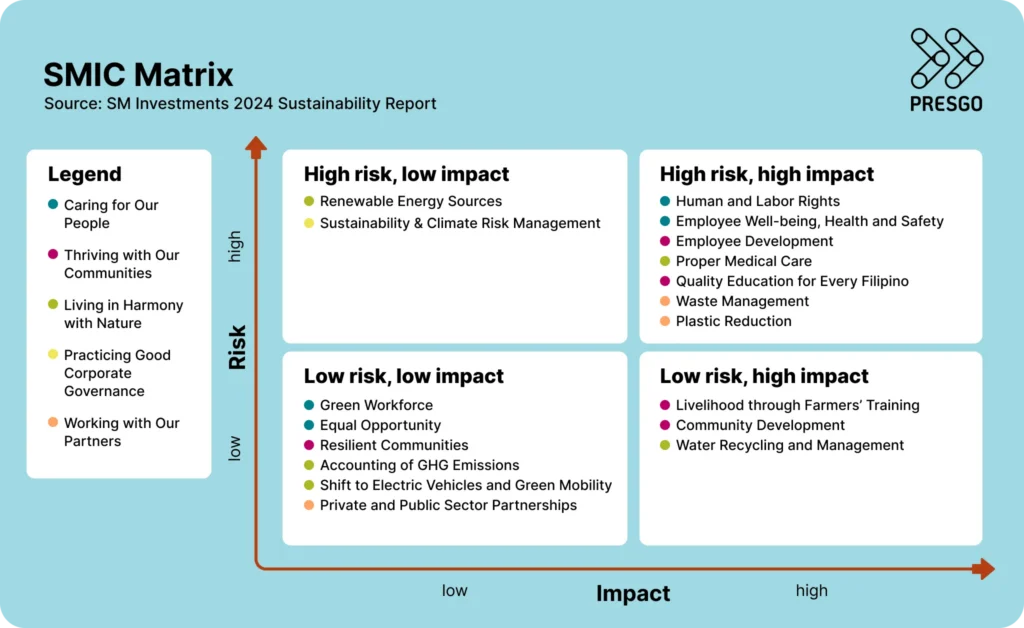

The SM Investments Corporation (SMIC) is one of the Philippines’ largest publicly traded groups that covers nationwide shopping mall operations, property developments, and commercial banks. Its SMIC ESG report anchors materiality work in ongoing engagement across five defined stakeholder groups, using both structured and day-to-day conversations to learn what matters most.

- People shape internal and workplace priorities around inclusion and risk.

- Customers ground materiality in product and service impact.

- Suppliers and business partners extend SMIC’s sustainability reach into its value chain, particularly MSMEs.

- Communities tie material topics to socioeconomic development.

- Investors anchor reporting in sustainable financial returns and transparency.

Inputs from these groups directly determine which sustainability topics get prioritized and how they connect to strategy. These priorities are validated and mapped in a quadrant, plotting each material topic depending on levels of risk and impact to the business.

Source: SM Investments Corporation 2024 Sustainability Report

4. Explicit connection to business risk and strategy

ESG risks become material when they affect the company’s supply chains, operations, finances, and regulatory standing. A strong materiality assessment shows that those direct and indirect connections clearly influence the company’s goals and decision-making.

A clear example is how the Ayala Corporation sustainability report links material topics to its strategy. Its climate action connects to ACEN’s renewable investments and the net zero target. Cybersecurity materiality resulted in a new appointment of a chief information security officer and a dedicated project office. Sustainable financial materiality is tied to US$6.2 billion raised since 2019 and the Sustainable Investing Framework, which requires environmental and social considerations at the Investment Committee level.

5. Expanding scope beyond single materiality

The PFRS S1 and S2 require a single materiality approach, specifically financial materiality, which discloses ESG risks and opportunities that could affect cash flows, access to finance, or cost of capital. Despite that, many leading Philippine companies voluntarily apply double materiality, which simultaneously assesses how their operations impact people and the environment.

This is visually presented in Manila Water’s materiality matrix above. While not a PFRS requirement, this broader approach adds depth and credibility to a materiality assessment, especially for companies with large value chain exposure or those targeting global markets. Ayala Corporation, Manila Water, and SM Investments Corporation are among the companies that already reflect this in their reporting.

6. Transparent methodology with clear thresholds

Companies should account for how they came up with the material topics, who they consulted, their scoring criteria, and the scope of their material topics. This documentation makes the process justifiable to auditors, investors, and regulators, especially since the SEC’s PFRS requirements are more stringent on materiality and disclosure quality. A clear scope and foundation process also allows for a long-term materiality approach, where companies continuously reaffirm and reevaluate their existing ESG priorities rather than starting from scratch in every report.

Transparent methodology matters most when the data is hardest to get. For many Philippine companies, the challenge that shows up most evidently in a value chain audit is outside their direct operations, which are scope 3 emissions.

How do leading Philippine companies approach scope 3 topics in their materiality assessments?

One of the most significant ESG risks for many Philippine companies is scope 3, or supply chain emissions. Supplier practices, upstream and downstream emissions, and logistical chains run through climate-vulnerable regions and provinces. These are the areas where disruption actually happens, but they’re also the areas most commonly left out or mentioned vaguely in sustainability reporting in the Philippines. Scope 3 emissions disclosures are not immediately required under the new PFRS sustainability standards. The SEC allows companies a transition period of up to two years before Scope 3 reporting becomes mandatory. However, many companies are already incorporating it in disclosures. Given its material impact on businesses, addressing scope 3 emissions should be viewed as a long-term risk management practice, beyond compliance.

- Ayala Corporation: The company reported their scope 3 emissions amounted to 97.1% of its 2024 overall footprint. They identified coal consumption from investments as the main reason for the increase from its 2021 baseline. To counter this, Ayala is pushing decarbonization across both ends of its value chain, encouraging suppliers toward cleaner practices and giving customers low-carbon options. Ayala Land’s move to green steel suppliers is one example, reducing upstream supply chain emissions. It is targeting a 29.4% cut in scope 3 by 2030 and 90% by 2050.

- Manila Water Company: Its sustainability report quantified scope 1, 2, and 3 emissions, with scope 3 representing 69% of its total footprint. Through their climate mitigation study, they traced the dominant sources to energy-related indirect emissions. The company has mainly focused its reduction efforts on scopes 1 and 2. In scope 3, their strongest contribution so far is transparency and methodology, which is already ahead of most Philippine company disclosures.

- SM Investments Corporation: The company was candid in its maturity gaps. Its 2024 scope 3 emissions data nearly tripled from its 2023 figure. This was primarily attributed to better data collection and disclosure on refrigeration and LPG consumption, instead of deteriorating emissions management.

These Philippine company ESG case studies show different stages of maturity in a thorough value chain audit and analysis. What separates these companies’ reporting from early-stage disclosures is that they report scope 3 data and explain what drives it. That materiality analysis is where disclosure becomes useful in decision-making. And with the trajectory and current global sustainability regulations, it is already an advantage to consider applying scope 3 in disclosures and materiality assessments.

Build a Successful ESG Materiality Assessment with Presgo

With the nearing PFRS adoption timeline, Philippine companies are navigating an increasingly demanding regulatory and stakeholder environment. Knowing what matters is the clearest competitive advantage in sustainability reporting in the Philippines. With clear materiality, adopting technology makes this entire process more manageable.

Presgo is an advanced ESG reporting software built to support exactly this kind of materiality-driven approach. Presgo is equipped with modular ESG tools and materiality solutions.

- AI-supported materiality assessment: Identify and prioritize material topics using structured analysis and AI-generated heatmaps that surface ESG issues with the highest business impact.

- Carbon calculator: Measure scopes 1, 2, and 3 emissions using verified emission factors from the GHG Protocol, IPCC, U.S. EPA, UK DEFRA, and IGES, with configurable surveys and automated summaries for scope 3 reporting.

- Supplier ESG engagement: Collect and assess supplier ESG data through custom surveys and AI-assisted scoring to strengthen Scope 3 supply chain compliance.

- Disclosure hub: Align reports with GRI, IFRS S1 and S2, CSRD, and the SEC’s local sustainability reporting requirements in one centralized platform.

- Real-time performance tracking: Monitor ESG targets and KPIs through interactive dashboards that flag gaps and track progress against your commitments.

The best sustainability reports in the Philippines have a clear materiality foundation. Request a demo today and start building yours with Presgo.