Contents

Recently, corporations have witnessed their transformations of environmental, social, and governance (ESG) initiatives from mere token ingredients of public relations statements to industry requirements. Regulatory bodies and policymakers have likewise deployed requirements and directives on how companies should measure and communicate their ESG-related efforts to the public.

In keeping with the strides of neighboring countries like Thailand, Malaysia, Hong Kong, and Singapore, the Philippines’ Securities and Exchange Commission (SEC) issued Memorandum Circular 4, also tagged as Sustainability Reporting Guidelines for Publicly-Listed Companies (PLCs), in early 2019. This required local PLCs to report their non-financial and sustainability performance. Then, in December 2025, the SEC’s Memorandum Circular 16, Series of 2025, now mandates structured guidelines that extend beyond PLCs to cover large non-listed entities (LNLs) as well.

For Philippine companies trying to navigate the SEC’s ESG-related mandates in sustainability reporting, this guide breaks it down.

What changed from the SEC’s MC 4 to MC 16 sustainability reporting?

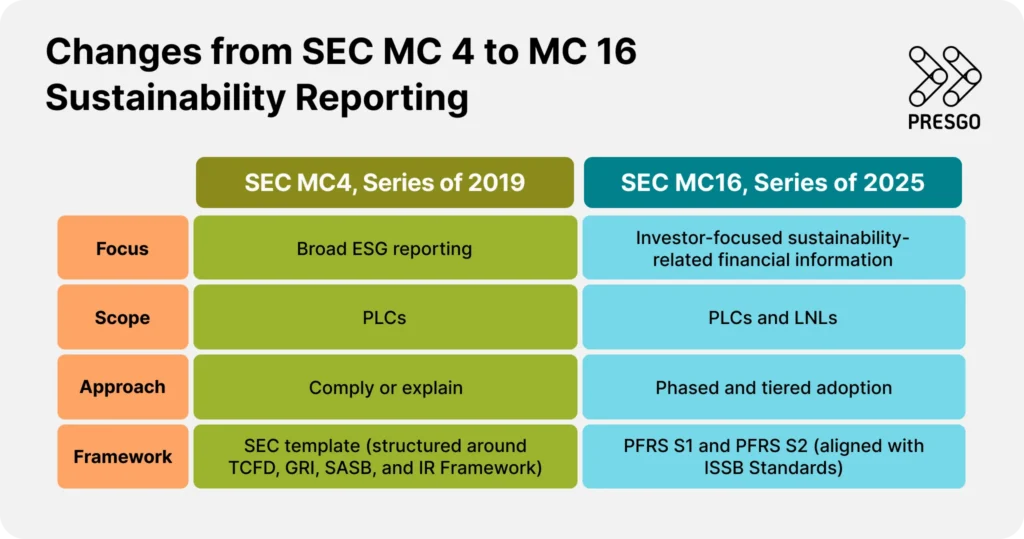

The SEC’s first sustainability reporting guidelines, Memorandum Circular 4, Series of 2019, were a starting point for the country’s focus on ESG. It offered organizations an inward look at their corporate efficiency and efficacy concerning their economic, environmental, and social risks, opportunities, and efforts. In the same vein, the Commission saw compliance with this mandate as an opportunity for companies to assess and measure their contributions towards the attainment of global sustainability initiatives like the 2030 United Nations Sustainable Development Goals and local development goals like AmBisyon Natin 2040.

The sustainability reporting from MC 4 was developed with the shared structures of global frameworks, such as the GRI, TCFD, SASB, and IR Framework. All PLCs were required to submit a sustainability report together with their annual reports. The first three years of the implementation adopted the “comply or explain” approach, meaning PLCs reported what they could and explained what they could not, with certain guidelines.

Since then, international standards have matured. The ISSB released its IFRS S1 and S2 standards, and neighboring ASEAN markets adopted them. The SEC’s MC 4 served its purpose, but the Philippines needed to close that gap with sustainability developments. The Memorandum Circular 16, Series of 2025, issued in December 2025, does exactly that, adopting the IFRS S1 and S2 structure in the Philippine Financial Reporting Standards (PFRS).

The PFRS S1 establishes the general guidelines for sustainability-related financial information reporting, while PFRS S2 is for climate-related reporting. Both standards are aligned with the ISSB framework and developed for the Philippine context. Under MC 16, PLCs, now including LNLs, are encouraged to begin transitioning to the SEC’s PFRS phased and tiered adoption timeline.

What is in the SEC’s Sustainability Reporting Template?

PFRS shifts the disclosure focus from a broad ESG topic checklist to investor-focused sustainability-related financial information. The framework involves risks and opportunities that carry real weight on a company’s cash flows, capital access, and long-term value, including a climate-related approach.

Under the new circular, sustainability reports must be reviewed and approved by the board of directors and submitted as an attachment to the annual report. Beginning FY 2026, the PFRS S1 and S2 standards will become a government requirement through a tiered roadmap depending on company size and market standing. PLCs under MC 4 and LNLs may continue to use any recognized international framework for their reports as long as they don’t contradict the PFRS standards.

Here are the key components that must be included in every PLC’s sustainability report:

Materiality assessment

Every organization has a wide array of ESG-related policies and issues on which it can report. The topics of environmental, economic, and social issues revolve around a multitude of aspects and processes. Sustainability reporting under PFRS S1 and S2 requires companies to identify and disclose the ESG topics that are material to them. Getting this foundation right in a materiality assessment shapes everything that follows: which disclosures are included, where the data comes from, and how the management approach narrative holds together.

The principle of materiality substantiates the relevant topics organizations need to report on. In identifying industry-specific topics, companies can look into the SASB-anchored materiality finder. Simply put, any matter or topic that has a consequential influence on various aspects of your company is considered material and warrants disclosure.

Companies are expected to detail their materiality process by explaining how they applied the materiality principle to determine their material topics. To help companies in their materiality assessment, the materiality matrix provides a graphic representation of a company’s material topics ranked according to importance.

In addition to the materiality process, PLCs and LNLs need to note that every disclosure should be backed by a narrative of their management approach. Ideally, the management approach needs to lay out the policies, commitments, responsibilities, targets, resources, grievance mechanisms, projects, initiatives, and programs to support the given material topic.

Mandatory External Assurance

Absent from MC 4 is external assurance, now a formal requirement under MC 16. Two years after each tier’s PFRS adoption begins, companies must obtain limited external assurance on their scope 1 and 2 GHG emissions. This assurance can come from an independent licensed accountant or qualified assurance provider following the International Standard on Sustainability Assurance (ISSA) 5000. The expectation is that this assurance will deepen disclosures over time as reporting matures.

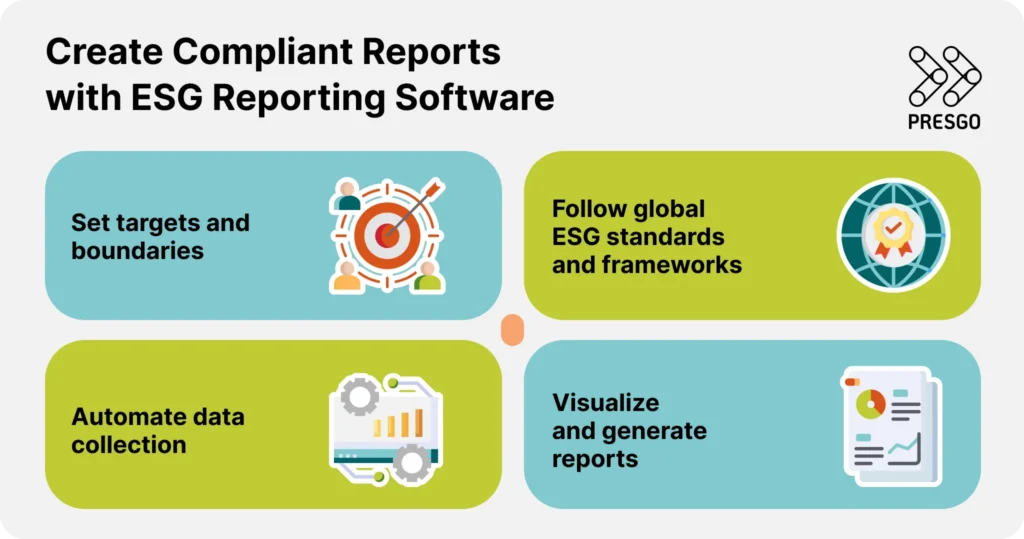

Create Compliant Reports with Presgo ESG Reporting Software

Staying ahead in the ever-evolving ESG landscape for PLCs and LNLs necessitates an ESG platform that enables your organization to analyze your ESG performance, benchmark against peers, and generate SEC-compliant reports.

Presgo is an AI-first reporting software made to simplify your materiality process and ESG journey — from efficient report preparation to generation. It allows automated collection workflows and a digital repository where years’ worth of data are consolidated for accuracy. Additionally, it provides full visibility and ownership of your data to monitor progress towards ESG goals and track processes.

Set targets and boundaries

Presgo allows you to set targets that are aligned with your goals and performance management practices. This reporting software offers a customizable dashboard where you have maximum visibility of your performance and that of other organizations. This makes it easier to benchmark against peers and set ESG goals based on the identified gaps.

A powerful ESG reporting platform can easily help you assess if you are on track with the ESG metrics and limitations you have set for your organization. With Presgo, you can color-code your goals as you input them for efficient tracking and follow-up.

Automate data collection

ESG data automation simplifies the data collection process and creates efficient workflows for you and your collaborators. You can do away with the laborious process of collating years of data from several sources and focus instead on strengthening your ESG efforts. You can also expect fewer human errors to get in the way of your compliance.

With Presgo, you are assured that your data is in one centralized location and is accessible to the relevant people in your team. Accuracy of data would be no point of worry, as Presgo also employs robust data validation processing that helps you match the data you have input with your hardcopy evidence.

Visualize and generate reports

An ESG reporting software is your apprentice in telling a compelling tale of your company’s ESG journey. Generate SEC-compliant sustainability reports with Presgo by translating hundreds of your sustainability data into digestible graphs and dashboards. It also supports report customization with templates that allow easy incorporation of the company brand and inputting of qualitative narratives. With Presgo, ensure the distribution of compelling ESG reports that resonate with investors and keep you ahead of the competition.

Reach out to us to know how Presgo can help you create stand-out reports compliant with the SEC requirements.